Arm's FY24Q3 covers calendar Q4 2023. The shares doubled soon after the release, raising the question of how much reflected fundamentals versus a limited public float.

Arm FY24 Q3 earnings highlights:

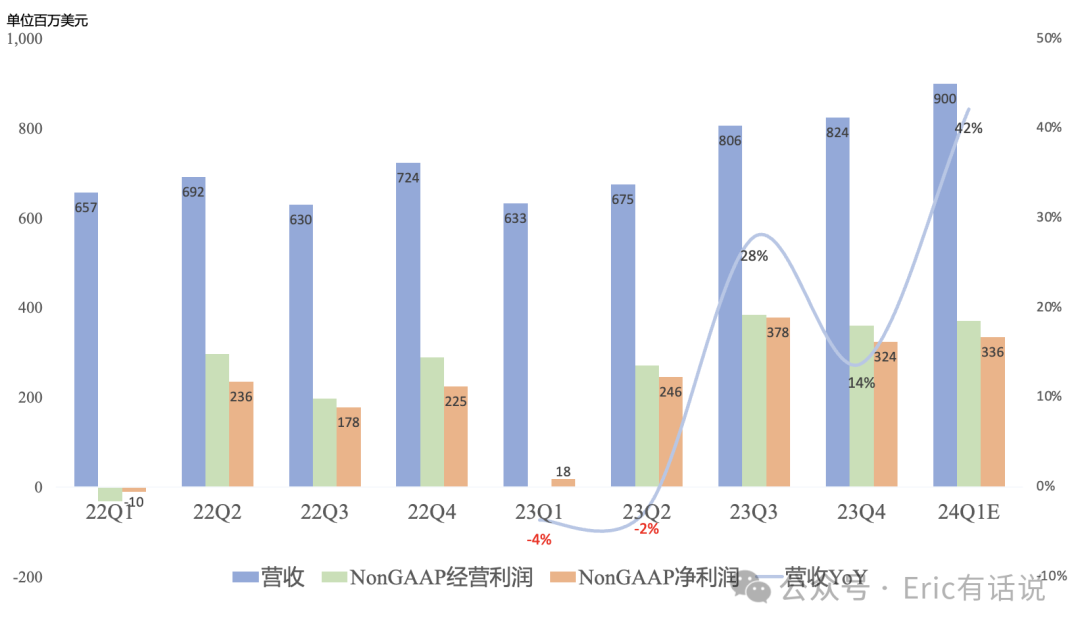

Revenue was $824M, up 14% year over year and 2% sequentially, marking the second consecutive quarter of record highs.

GAAP gross margin was 95.6%, maintaining a historical high, arguably the highest globally (CDNS 90.3%, Moutai Q3 91.5%).

GAAP operating income was $134M, down 45% year over year; GAAP operating margin was 16%.

Non-GAAP operating income was $361M, up 25% year over year; Non-GAAP operating margin was 44%, placing it in the top tier of semiconductors.

GAAP net income was $87M, down 52% year over year; Non-GAAP net income was $324M, up 44% year over year; Non-GAAP net margin was 39%, placing it in the top tier of semiconductors.

Despite Arm's near-100% gross margin, GAAP operating income remains low and was frequently negative in the past, primarily due to high R&D expenses at 52% of revenue, averaging 50% over the last eight quarters, which is also the highest level across the semiconductor industry.

Business Segments:

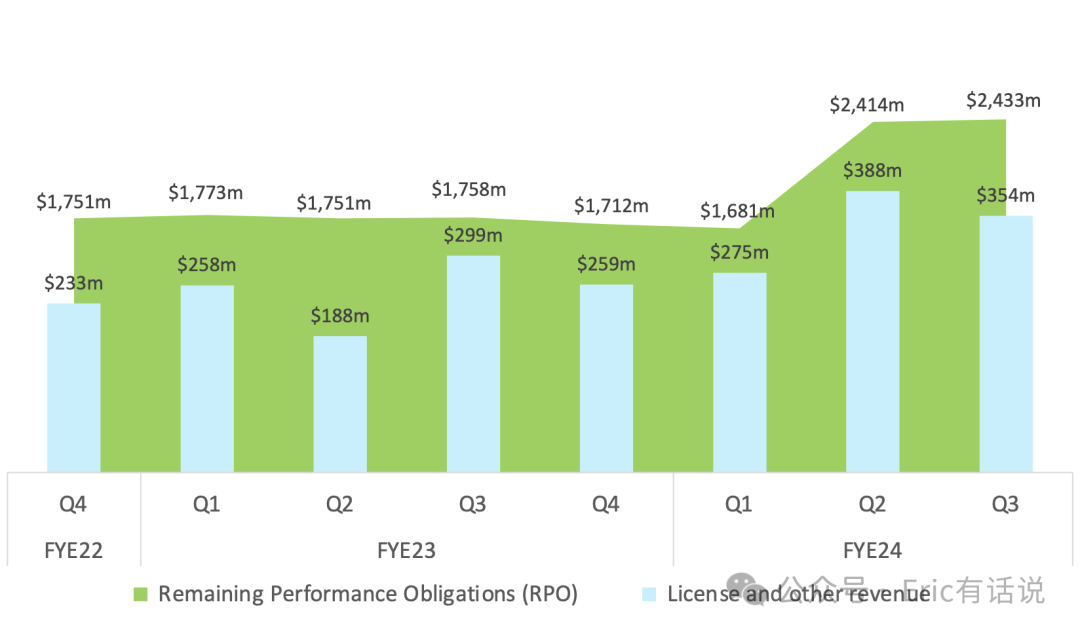

License & Other revenue was $354M, up 18% year over year and down 9% sequentially.

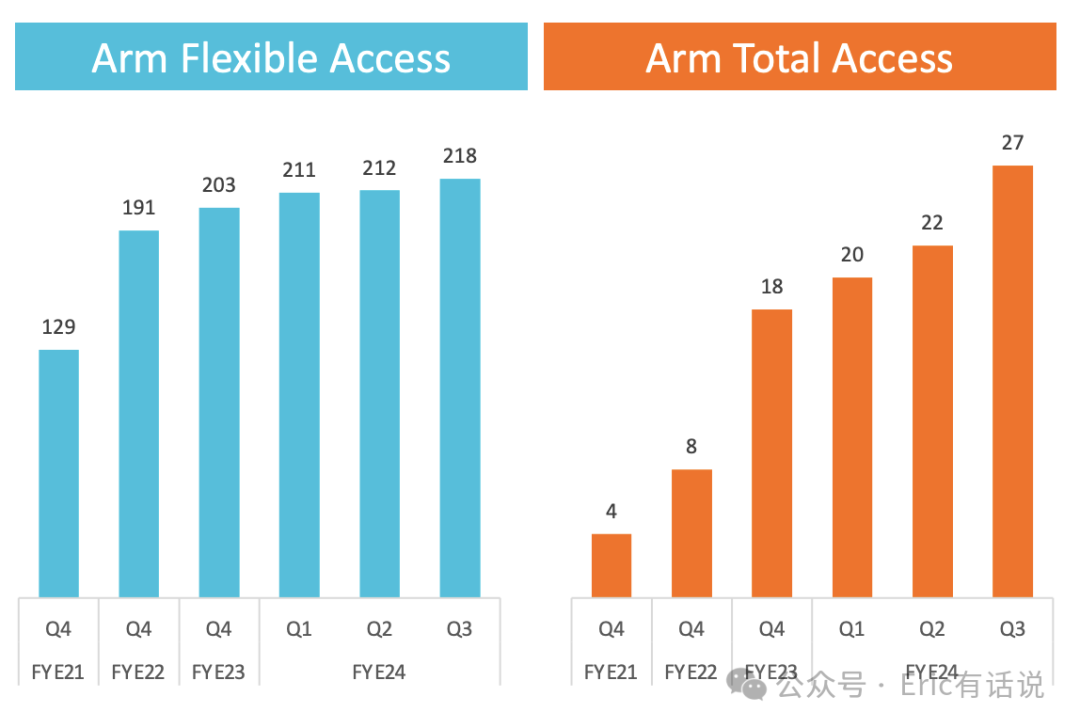

Five Arm Total Access (ATA) agreements were signed this quarter, bringing the cumulative total to 27, covering half of the top 20 customers; three of these were upgrades from Arm Flexible Access (AFA), with a few more expected next quarter.

Book-to-bill has exceeded 1 for two consecutive quarters; typically 40%-50% of license revenue comes from backlog.

AFA requires annual renewal; over 50 were renewed this quarter, 14 new agreements signed, net increase of 6, bringing the cumulative total to 218; AFA shows a long-term trend of upgrading to ATA, similar to the Microsoft Office 365 E3-to-E5 upgrade trend.

Data center licensing agreements have a quicker sales cycle time than traditional agreements.

ACV was $1.16B, up 15% year over year; RPO was $2.433B, up 38% year over year, of which 28% will be recognized in the next 12 months and 26% in months 13-24.

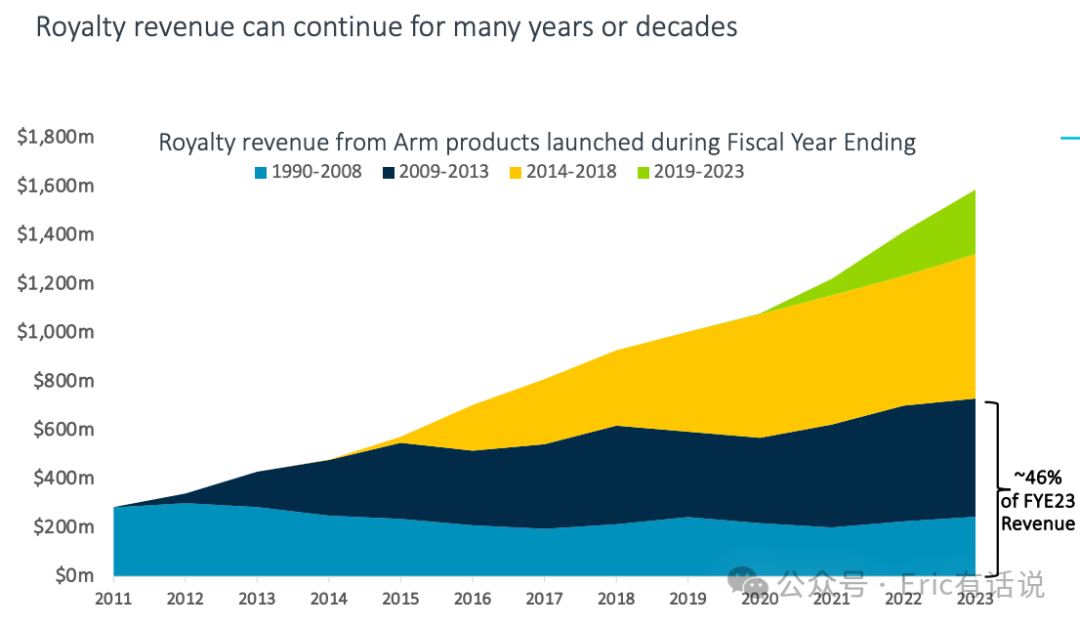

Royalty revenue was $470M, up 11% year over year and 12% sequentially, setting a new record.

The smartphone market is recovering, with significant year-over-year growth, accounting for 35% of royalty revenue; Arm v9 value per unit is double that of v8, and v9-related revenue rose from 10% of royalty revenue last quarter to 15% this quarter; over the next 3-4 years smartphones will fully transition to v9, currently primarily covering flagship devices; the v7-to-v8 transition took 3 years to reach 80%-90% penetration.

Cloud server revenue grew significantly year over year; new products are almost entirely v9-based.

Automotive ADAS royalty revenue grew year over year; automotive MCU royalty revenue declined year over year; IoT/embedded was flat year over year.

Arm FY24 Q3 earnings call highlights:

Arm China was the largest growth driver this quarter, with strong automotive and data center demand; Arm China revenue share rose from 20% last quarter to 25% this quarter; a large gap exists between Arm China revenue and related-party revenue this quarter, mainly due to a one-time additional license (approximately 5% of total revenue); Arm China revenue share is expected to decline to the teens in the future.

Next quarter revenue is guided at $900M, up 42% year over year, exceeding expectations; royalty revenue is easier to forecast than license; next quarter royalty revenue is expected to grow mid-single digits sequentially and over 30% year over year, driven by rapidly rising Arm v9 penetration.

The first compute subsystems customer is Microsoft Cobalt, with a 128-core Neoverse CPU; AI growth comes primarily from data centers (NVIDIA Grace Hopper + Microsoft Cobalt 100 + Amazon AWS Graviton), not smartphones.

Whether Arm's current valuation is reasonable can be assessed by comparing to semiconductor SaaS peers such as SNPS (24E P/S 13x, 24E Non-GAAP PE 42x) and CDNS (24E P/S 18x, 24E Non-GAAP PE 51x) to derive a near-term fair valuation range for Arm.

For near-term earnings, using the next-quarter $900M revenue guidance as a conservative run rate yields $3.6B annualized; assuming 40% full-year year-over-year growth yields $4.1B. Based on the average Non-GAAP net margin of 40% over the last four quarters, net income would correspond to $1.44-1.64B.

Under these assumptions, Arm's near-term fair valuation is approximately $60-90B, while its current $145B market cap would require explosive earnings growth to justify.

In a previous article I noted:

This quarter, NVIDIA Grace Hopper / Microsoft Cobalt 100 / Amazon AWS Graviton indeed delivered strong results. Driven by AI, Arm server CPU market penetration is poised to accelerate. However, Arm still needs a blowout earnings report to prove its high valuation; 40%+ revenue growth is far from sufficient.