Arm's FY25Q3 covers October through December 2024.

Arm FY25Q3 Key Takeaways:

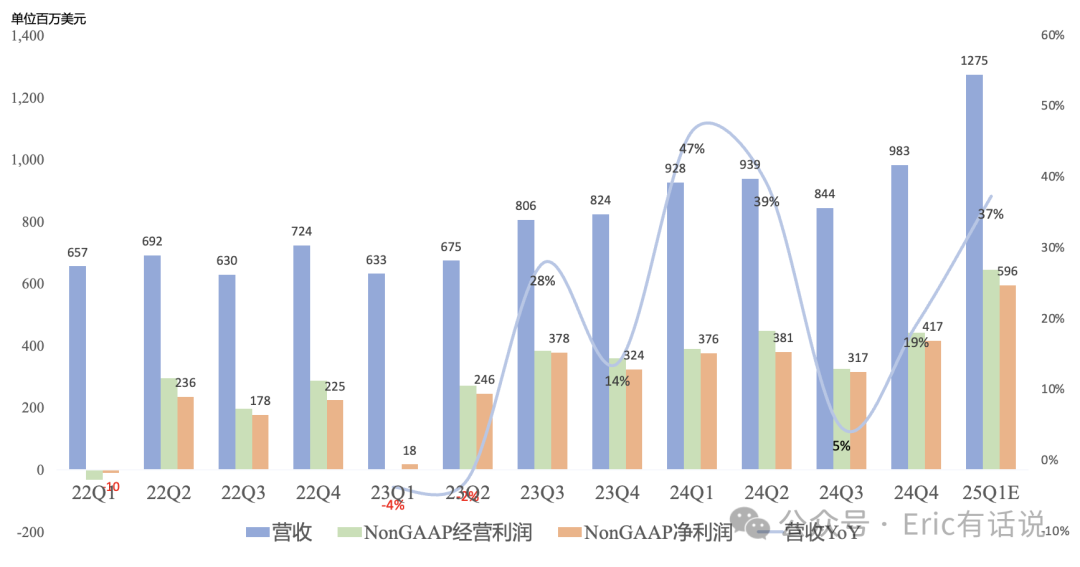

Revenue $983M, up 19% YoY, up 16% sequentially;

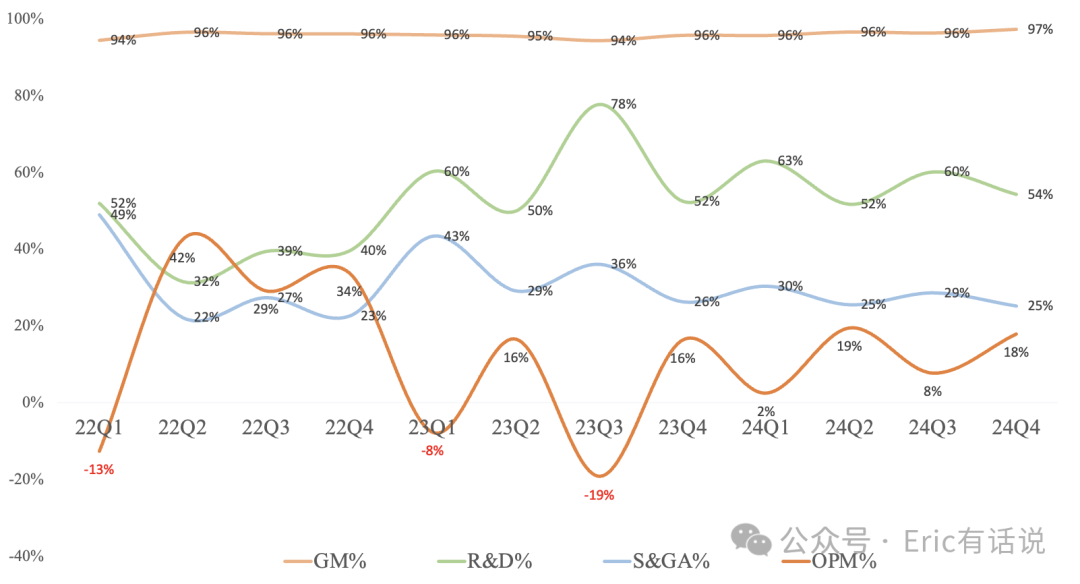

GAAP gross margin 97.2%, still the highest globally;

GAAP operating income $175M, up 31% YoY, up 173% sequentially, GAAP operating margin 18%;

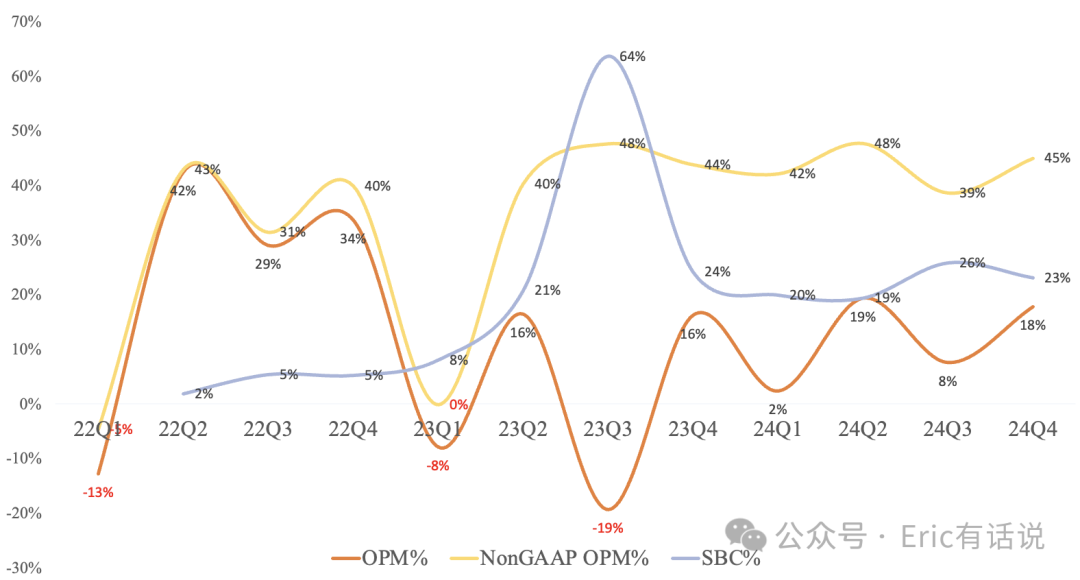

Non-GAAP operating income $442M, up 22% YoY, up 36% sequentially, Non-GAAP operating margin 45%, among the top globally;

GAAP net income $252M, up 190% YoY, up 136% sequentially, GAAP net margin 26%;

Non-GAAP net income $417M, up 8% YoY, up 32% sequentially, Non-GAAP net margin 42%, among the top globally;

Even though Arm boasts a gross margin near 100%, its GAAP operating profit remains very low, and it frequently posted losses in the past. The main reason is elevated R&D expense, which accounted for 60% of revenue this quarter, while sales and marketing expense accounted for 29%. However, after stripping out the sizable stock-based compensation, the non-GAAP operating margin has held around 40%.

Business Segments:

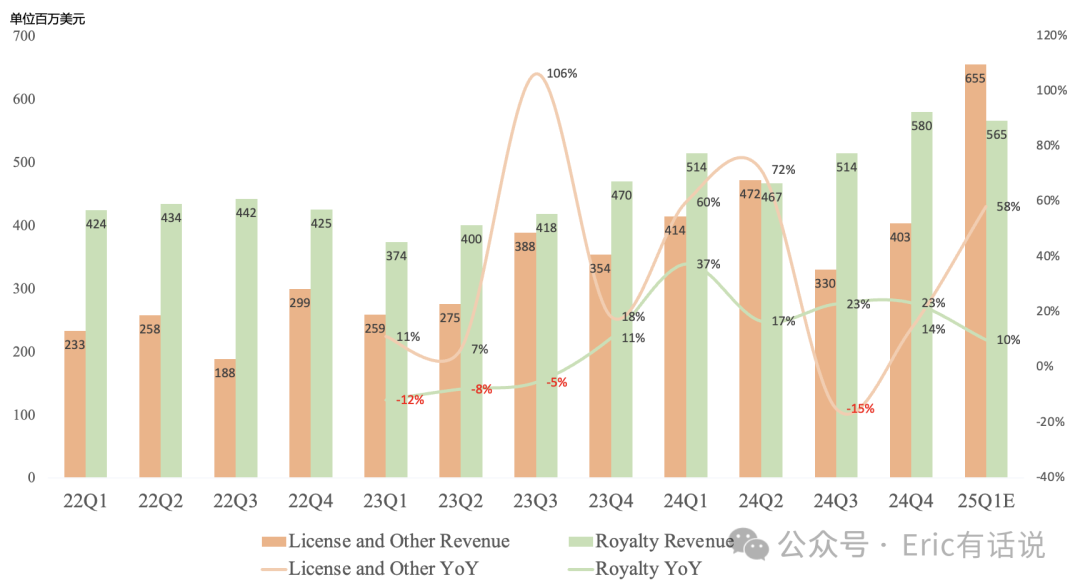

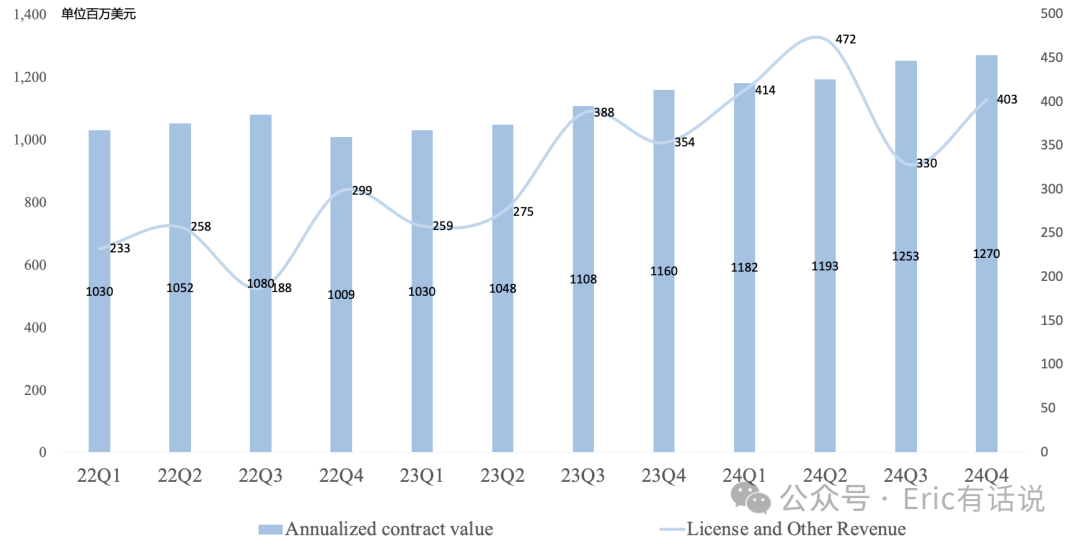

License & Other revenue was $403M, up 14% year over year and 22% sequentially.

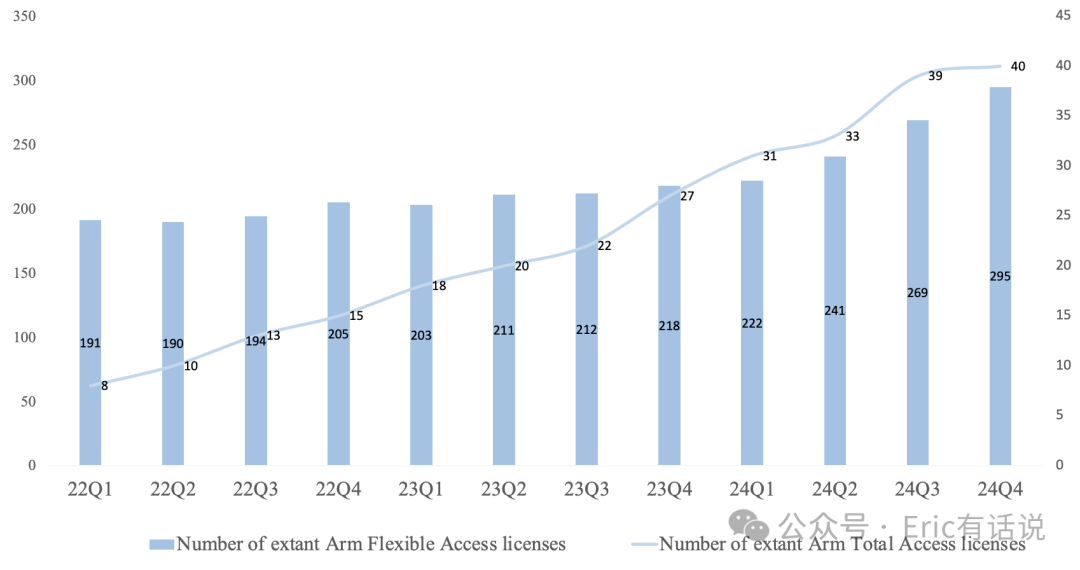

The company signed one Arm Total Access (ATA) agreement this quarter, bringing the cumulative total to 40, covering half of the top 30 customers. Arm Flexible Access (AFA) now has 295 customers. ATA annual fees increase 7% each year on a three-year renewal cycle. Because ACV historically came mainly from ATA, its growth rate was also around 7%. In the AI era, ACV benefits not only from ATA but also from CSS and Armv9, so ACV growth can reach 14%-15%.

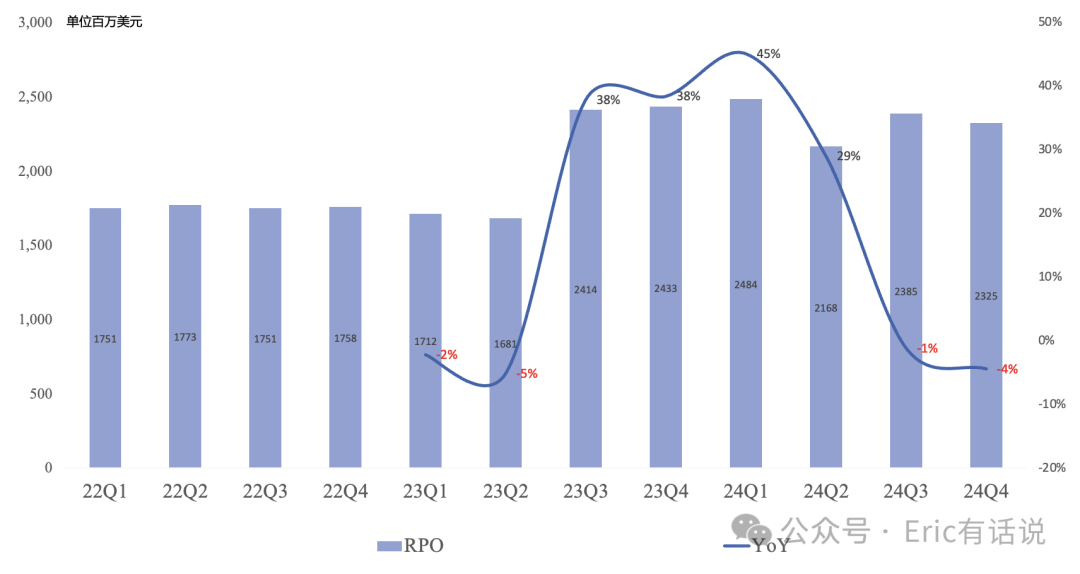

ACV was $1.27B, up 9% year over year and 1% sequentially. RPO was $2.325B, down 4% year over year, marking the second consecutive quarter of year-over-year decline, and down 3% sequentially. Of the RPO, 28% will be recognized as revenue within the next 12 months and 17% within 13-24 months.

FY25 License revenue is expected to grow nearly 30% year over year (slightly raised).

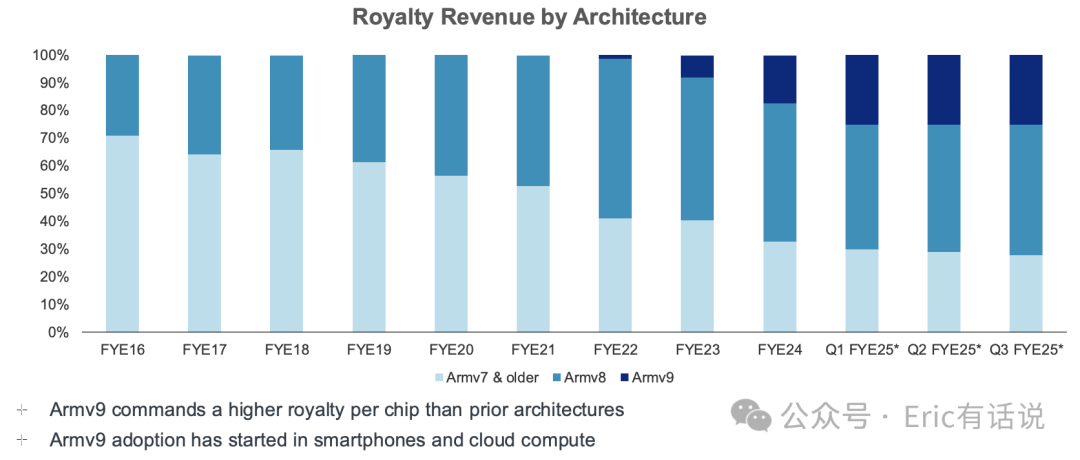

Royalty revenue was $580M, up 23% year over year and 13% sequentially.

Armv9-related revenue as a percentage of royalty revenue held at 25% for the past two quarters, unchanged, falling short of management's prior expectation of sequential increases. Management still expects Armv9's long-term share to reach 60%-70%. Royalty growth was driven primarily by Armv9 penetration and CSS customer chip ramps (Dimensity 9400, Cobalt), with signs of recovery in the IoT market. The CSS royalty rate is twice that of Armv9, which in turn is twice that of v8.

This quarter, the company's smartphone royalty revenue growth again exceeded the growth in smartphone customer shipments. FY25 full-year royalty revenue is expected to grow in the high-teens year over year (unchanged).

Arm FY25Q3 Earnings Call Highlights:

Next quarter revenue is guided to $1.175B-$1.275B, up 27%-37% year over year. Non-GAAP net income is guided to $511M-$596M, up 36%-58% year over year.

FY25 full-year revenue is guided to $3.94B-$4.04B (low end raised, high end lowered), up 18%-27% year over year. Non-GAAP net income is guided to $1.66B-$1.745B (low end raised, high end lowered), up 25%-32% year over year.

Related-party revenue (primarily Arm China) grew 48% sequentially. Arm China accounts for roughly 25% of revenue and 20% of ACV. Arm China's revenue share is expected to decline to the mid-teens over the long term, but the share will not change significantly over the next few quarters.

Arm's Core Growth Formula

It has long been emphasized that Arm's biggest problem is growth that is too low, while its greatest strength is high predictability. Management signaled future margin improvement; combined with the prior FY27 $6B revenue guide, non-GAAP net income could challenge $3B, implying a fair valuation of $100B–$150B. Given the limited float, rumors of an Ampere acquisition, and the possibility of SoftBank cashing out to invest in OpenAI, Arm's share price has always been volatile.