Arm's FY24Q4 covers January through March 2024.

Arm FY24Q4 Earnings Highlights:

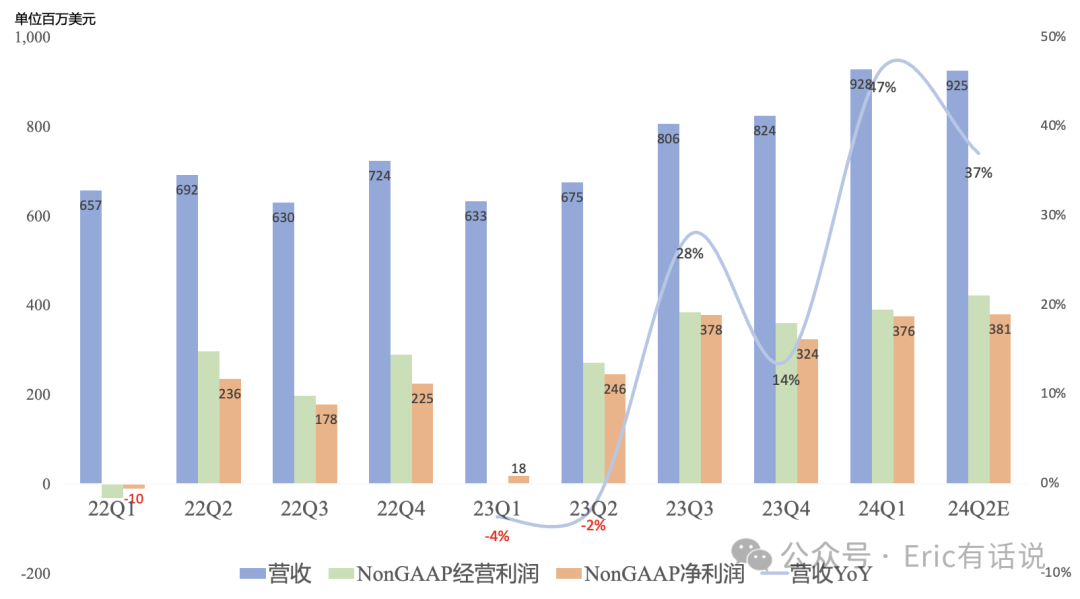

Revenue was $928M, up 47% year over year, up 13% sequentially, a record high for the third consecutive quarter.

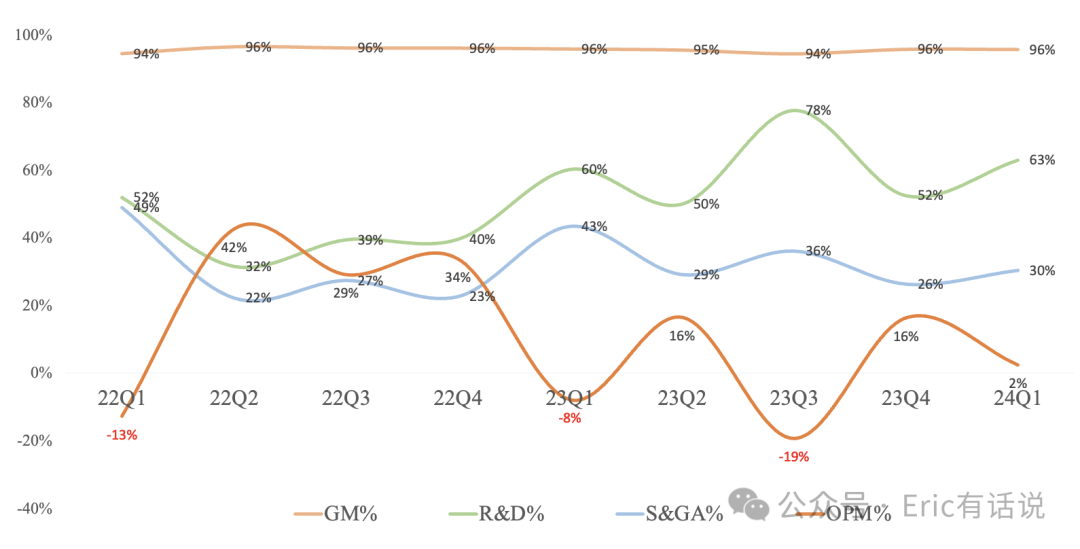

GAAP gross margin 95.6%, still the highest globally (CDNS 87.6%, Moutai 92.7%).

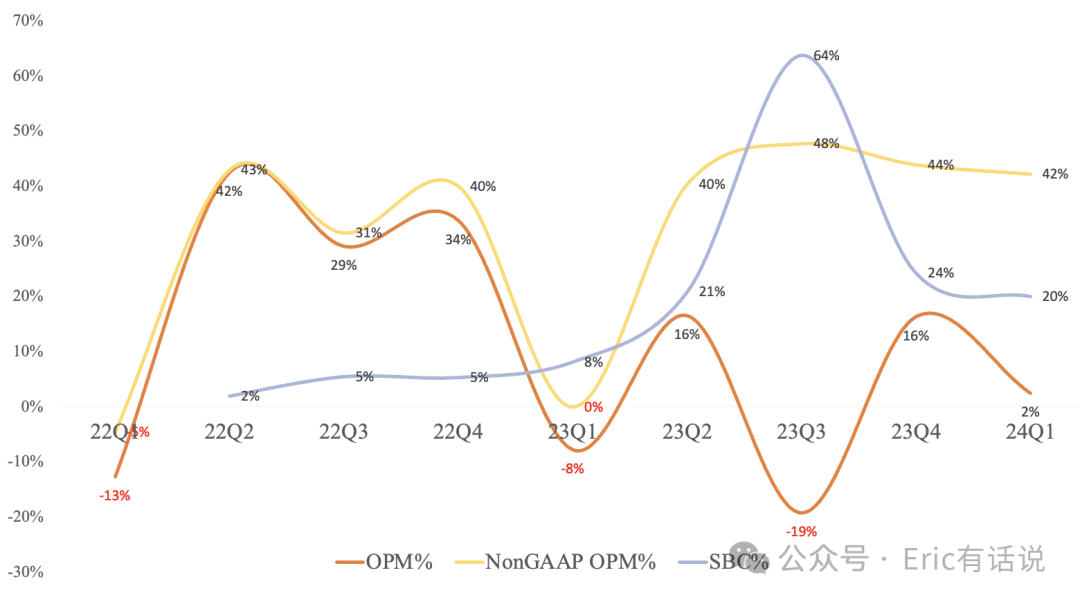

GAAP operating income was $22M, swinging from a loss year over year, down 84% sequentially; GAAP operating margin was 2%.

Non-GAAP operating income was $391M, swinging from a loss year over year, up 8% sequentially, a record high; Non-GAAP operating margin 44%, at the top of the semiconductor sector.

GAAP net income was $224M, up 737% year over year and 157% sequentially. Non-GAAP net income was $376M, up 1,325% year over year and 16% sequentially; non-GAAP net margin was 41%, placing it among the semiconductor leaders.

Despite near-100% gross margin, GAAP operating income is very low, often a loss previously, mainly due to high R&D at 63% of revenue this quarter, and SG&A at 30%; but stripping out high stock-based compensation, Non-GAAP operating margin holds at a high 40%.

Business Segments:

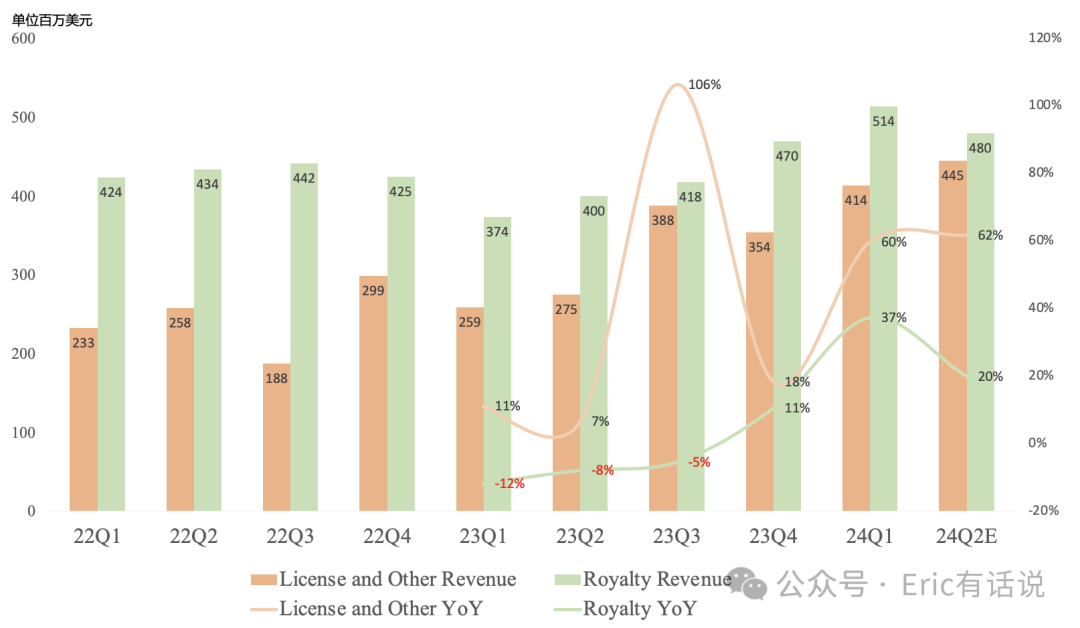

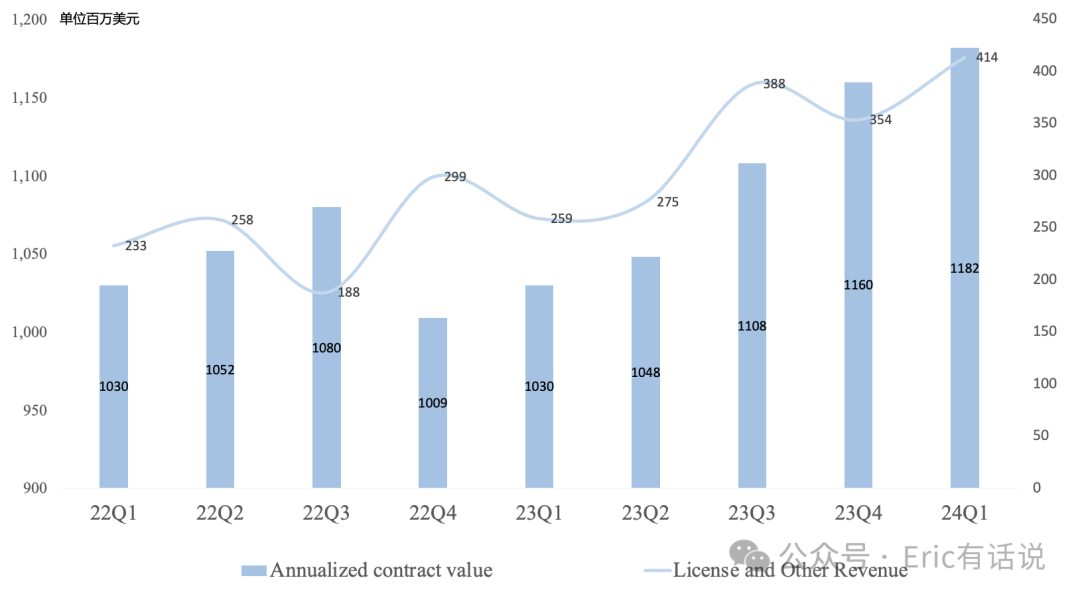

License & Other revenue was $414M, up 60% year over year, up 17% sequentially, a record high.

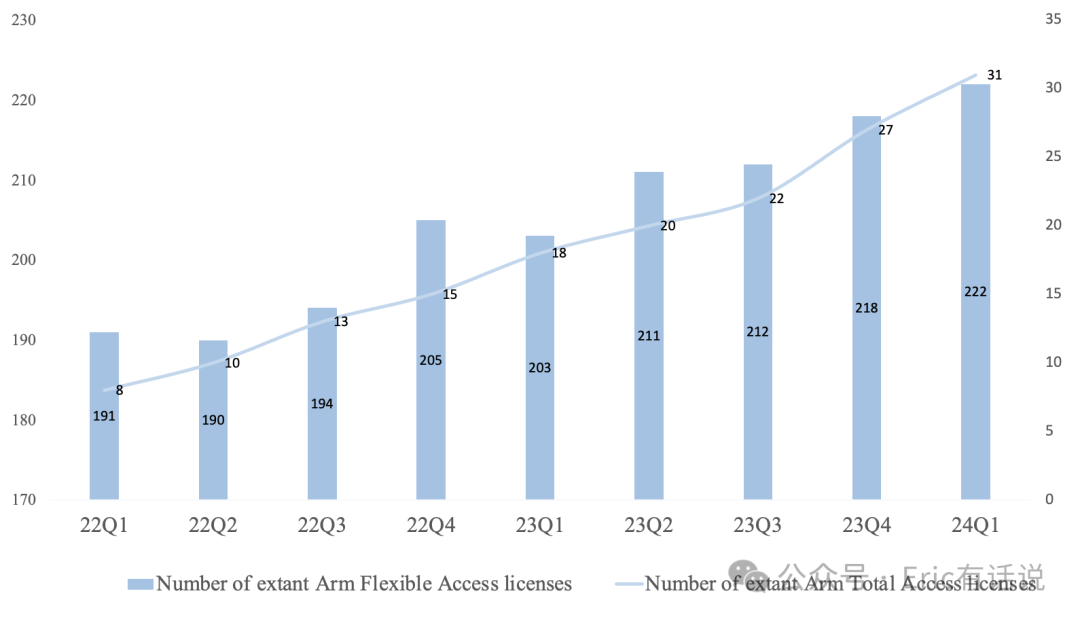

Signed 3 Arm Total Access (ATA) agreements this quarter, cumulative 31 agreements covering half of the top 20 customers; future target is 80% of customers on Arm Total Access (ATA).

Because AI software is evolving rapidly, AI hardware must accelerate iteration to keep up, driving accelerated Licensing growth; this quarter's Licensing revenue growth was primarily driven by increased AI chip investment.

Typically License revenue converts to Royalty 2-3 years later; large ATA Licensing converts to Royalty at a very high rate.

ACV $1.182B, up 15% year over year; RPO $2.484B, up 45% year over year, of which 28% recognized within 12 months, 14% within 13-24 months; expect full-year ACV to maintain low double-digit growth.

Royalty revenue was $514M, up 37% year over year, up 9% sequentially, a record high.

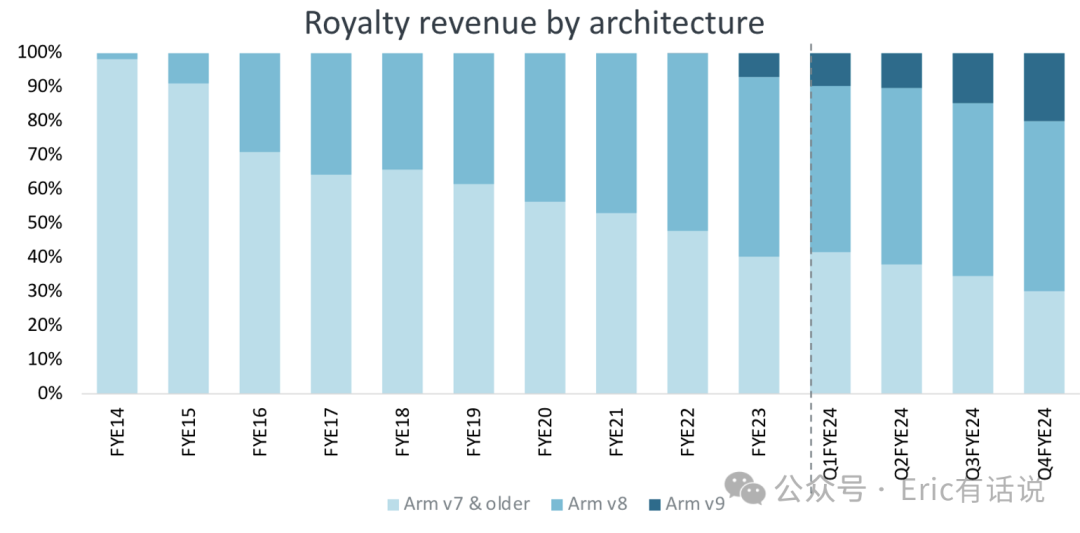

Armv9-related revenue as a share of Royalty revenue rose from 15% last quarter to 20% this quarter, expected to rise ~5 percentage points per quarter thereafter, reaching 60%-70% in 2-3 years.

This quarter's Royalty growth driven by rising Armv9 penetration across all end markets (phones, data center more pronounced), plus more CPUs inside chip, driving further Royalty growth.

Customer average shipments up ~2% year over year this quarter (company Royalty revenue up 37% year over year); expect next quarter customer average shipments up ~5% year over year (company Royalty revenue to grow ~20% year over year), showing large price/mix variance.

Compute Subsystems launched Neoverse V3 CSS this quarter; first automotive CSS in customer discussions; first CSS customer Microsoft Cobalt ramping; CSS demand far exceeds expectations, every end market wants CSS, expected to become a major Royalty business in 3-4 years.

Arm FY24Q4 Earnings Call Highlights:

Guided next-quarter revenue of $925M, up 37% year over year; Royalty revenue expected to grow 20% year over year, driven by rising Armv9 penetration, smartphone market recovery, and data center/automotive share gains, partially offset by continued weakness in IoT/industrial/networking; License & Other revenue expected to grow 60%+ year over year.

FY25 full-year revenue is guided to $4.1B, up 27% year over year; non-GAAP net income $1.7B, up 32% year over year; ACV to grow low double digits. Because licensing revenue recognition timing varies, H1 is expected to be 40% (Q2 lowest), H2 60% (Q4 highest). Backlog visibility is high, with full-year bookings expected to complete 60% of last year's level. Full-year royalty revenue is guided to grow mid-20s% year over year.

Guided FY25-FY27 revenue CAGR >20%; Royalty to exceed 75% of total revenue in several years.

Expect multiple Arm-based PC chips in the next 1-3 years; Arm PC share to rise noticeably in 2-3 years.

AI growth mainly from data center (NVIDIA Grace + Microsoft Cobalt 100 + Amazon AWS Graviton + Google Axiom, etc.).

Comparing to SNPS (24E P/S 13x, 24E Non-GAAP P/E 41x) and CDNS (24E P/S 17x, 24E Non-GAAP P/E 48x), two semiconductor SaaS stocks, yields Arm's near-term fair valuation range.

Arm's full-year revenue guide of $4.1B matches my prior estimate; Non-GAAP net income guide slightly higher at ~$1.53-1.75B. Based on that, Arm's near-term fair valuation is ~$70-90B. Given Arm's unassailable moat and management's FY27 guide, FY27 revenue ~$6B, Non-GAAP net income ~$2.6B, implying long-term valuation of $100-130B.

That said, Arm's guided 20% CAGR is far from enough to prove itself. TSMC's AI revenue exposure this year is conservatively estimated at $9B, and its management guides for 50%+ CAGR over the next 5 years.