Arm's FY25Q1 covers April through June 2024.

Arm FY25Q1 Earnings Highlights:

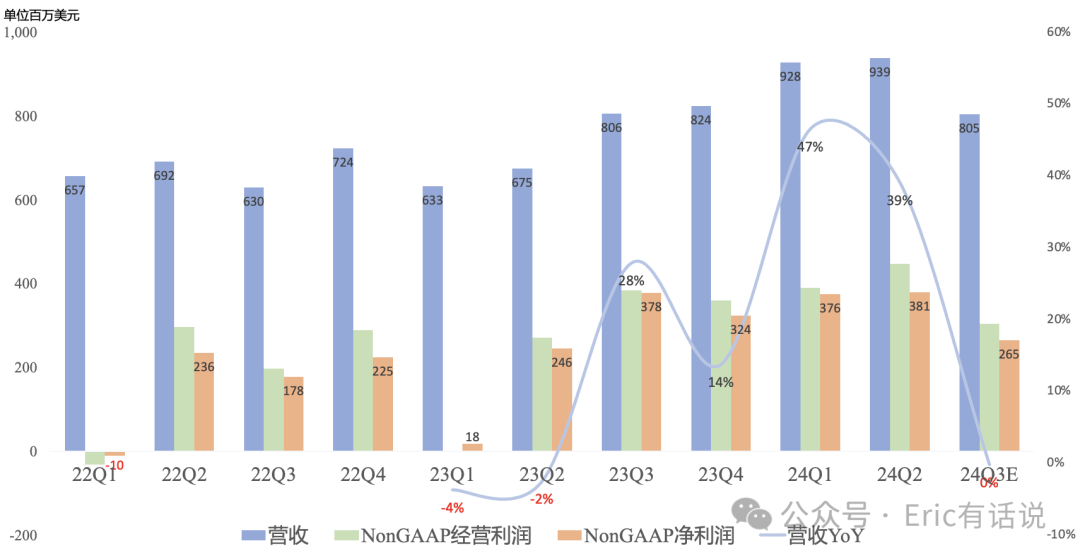

Revenue $939M, up 39% year over year and 1% sequentially, 4th consecutive quarterly record.

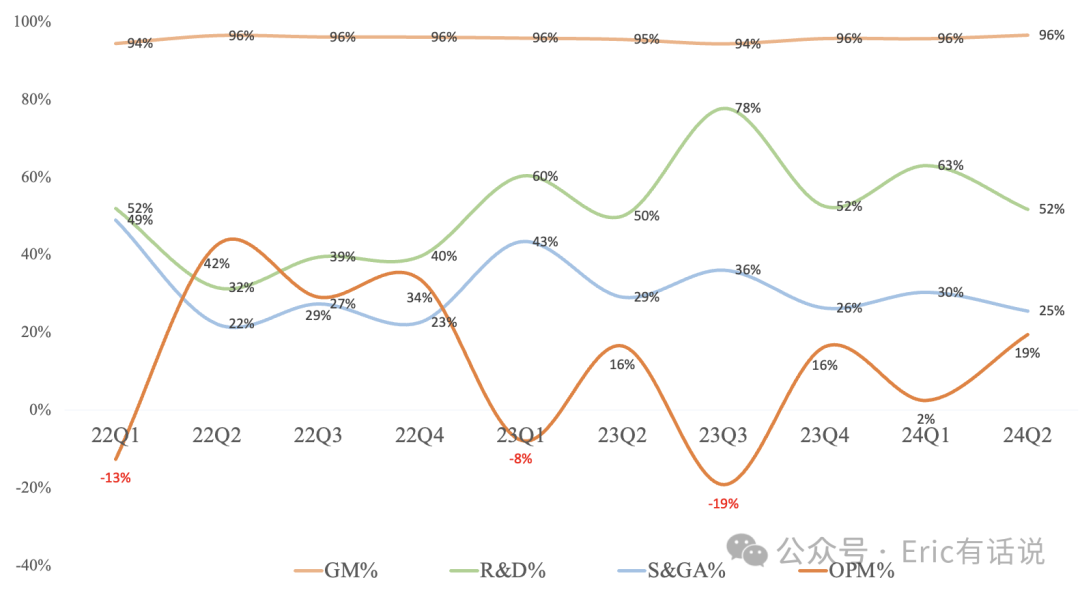

GAAP gross margin 96.5%, still the highest globally (CDNS 86.9%, Moutai 92.7%).

GAAP operating income $182M, up 64% year over year and 727% sequentially; GAAP operating margin 19%.

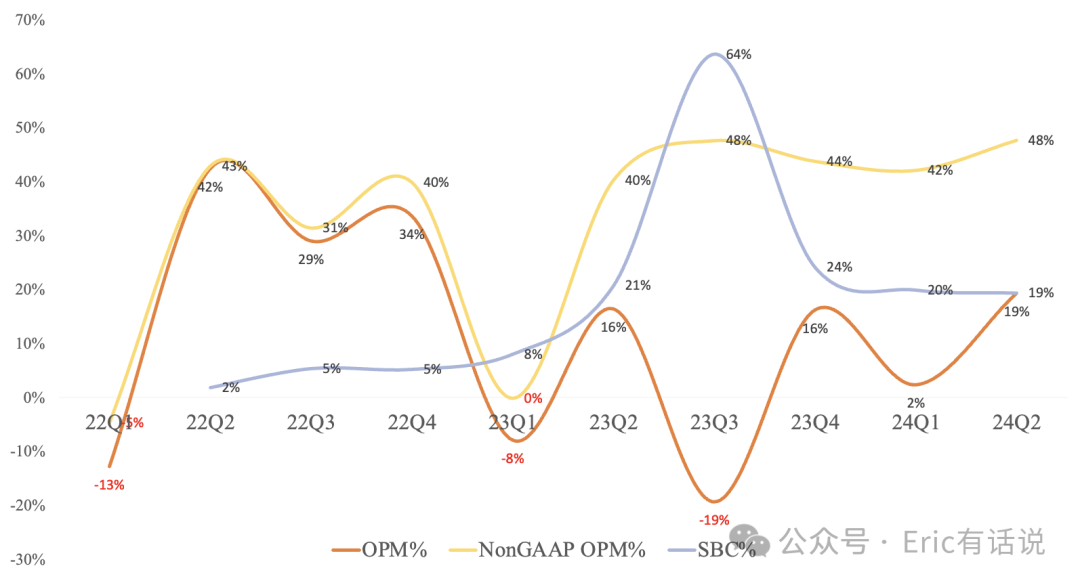

Non-GAAP operating income $448M, up 65% year over year and 15% sequentially, 2nd consecutive quarterly record; Non-GAAP operating margin 48%, among the top tier globally for semiconductors.

GAAP net income $223M, up 112% year over year, flat sequentially; GAAP net margin 24%.

Non-GAAP net income $381M, up 11% year over year and 1% sequentially; Non-GAAP net margin 41%, among the top tier globally for semiconductors.

Despite near-100% gross margins, Arm's GAAP operating profit remains low, often negative historically, mainly due to high R&D spend — 52% of revenue this quarter — and sales & marketing at 25%. However, stripping out the large stock-based compensation, Non-GAAP operating margin holds at a high 40%.

Business Segments:

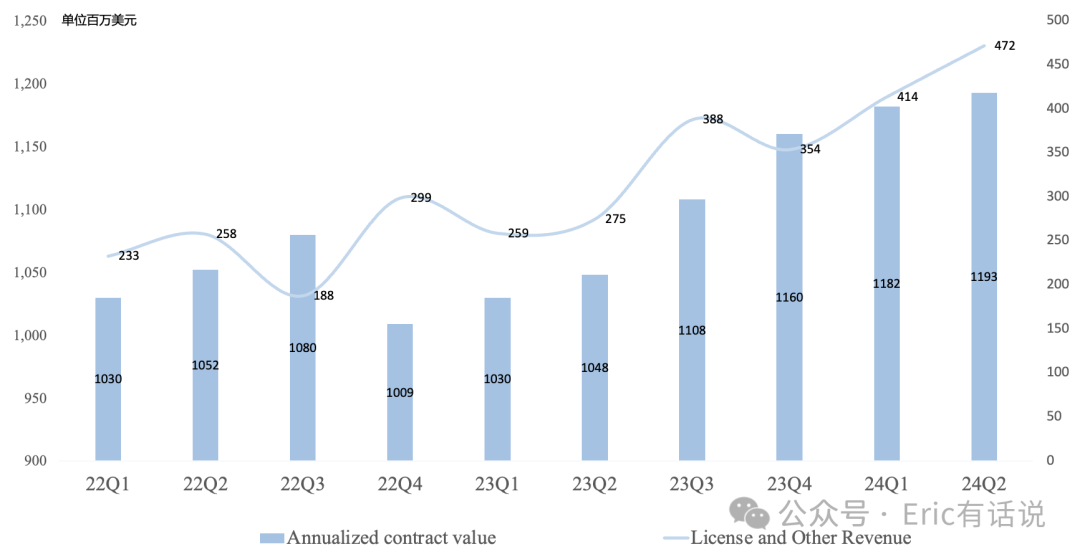

License & Other revenue $472M, up 72% year over year and 14% sequentially, 2nd consecutive quarterly record.

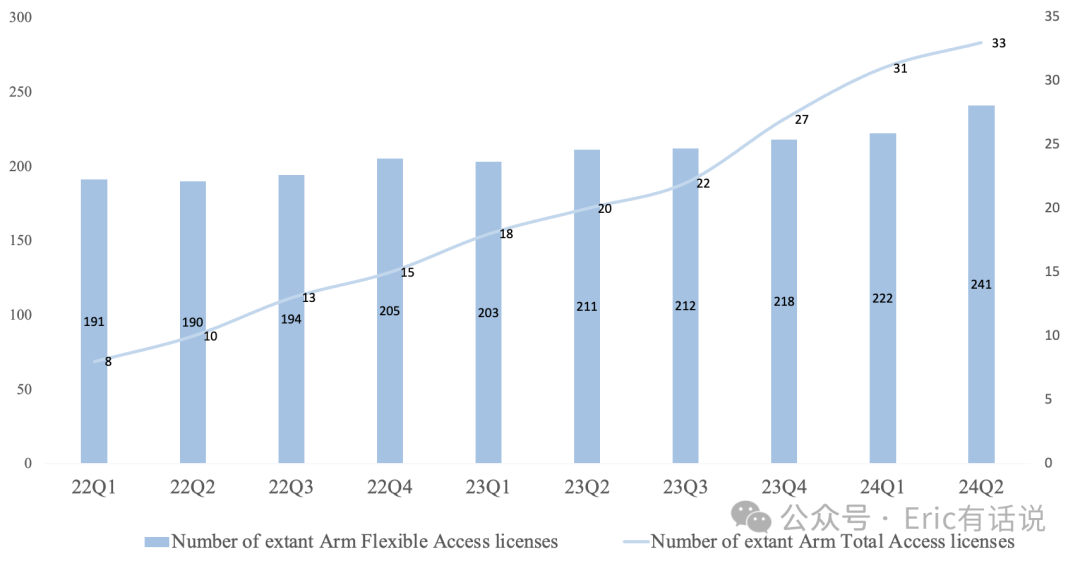

The company signed two Arm Total Access (ATA) agreements this quarter, bringing the cumulative total to 33, covering more than half of the top 30 customers; Arm Flexible Access (AFA) has been opened to mainland China, with 241 cumulative customers.

ACV was $1.193B, up 14% year over year and 1% sequentially; RPO was $2.168B, up 29% year over year but down 13% sequentially, of which 22% will be recognized as revenue within the next 12 months and 14% within months 13-24; full-year ACV is expected to maintain low-double-digit growth.

Q2 Licensing revenue growth is expected to be the full-year low point, as Licensing revenue is affected by recognition timing while bookings remain strong; Q4 Licensing revenue growth is expected to be the full-year high point; FY25 full-year Licensing revenue is expected to grow low to mid-20% year over year.

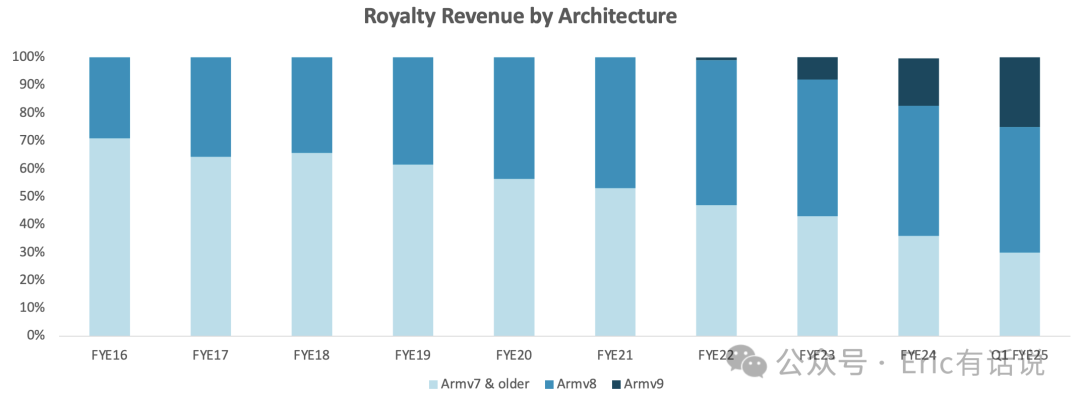

Royalty revenue was $467M, up 17% year over year and down 9% sequentially.

Arm V9-related revenue as a share of Royalty revenue rose from 20% last quarter to 25% this quarter, with mobile V9 accounting for 50%.

Mobile customers' average shipments grew single digits year over year this quarter, but the company's mobile Royalty revenue grew 50%+ year over year, data center Royalty revenue grew 75% year over year, and automotive Royalty revenue grew 20% year over year.

Typically License revenue generates Royalties 2-3 years later; phones fastest, datacenter and automotive slower; Royalty rate: CSS > v9 > v8.

Q2 Royalty revenue is expected to grow low-20% year over year (previously mid-20%); FY25 full-year Royalty revenue is expected to grow low-20% year over year, benefiting from rising Arm V9 penetration, data center and automotive share gains, and CSS customer chips ramping in the second half, while IoT, industrial, and networking markets remain weak and weigh on revenue.

Arm FY25Q1 Earnings Call Highlights:

Next quarter revenue is guided at $780M-$830M, down 5% to up 1% year over year; License & Other revenue is expected to decline 20%+ year over year due to Licensing recognition timing; Royalty revenue is expected to grow 20%+ year over year.

FY25 full-year revenue is guided at $3.8B-$4.1B, up 18%-27% year over year; Non-GAAP net income is guided at $1.5B-$1.7B, up 16%-32% year over year.

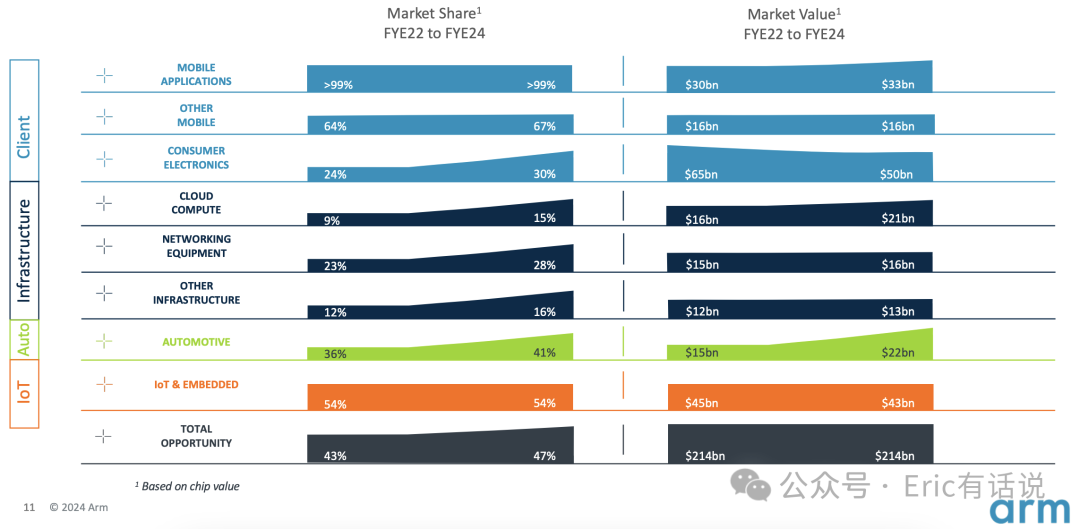

AI growth is primarily driven by data centers (NVIDIA Grace, Microsoft Cobalt 100, Amazon AWS Graviton, Google Axion, etc.), with Cloud Compute market share rising to 15%.

Arm's biggest issue remains low growth; its biggest advantage is high stability.