Lattice leads global shipments of low-power FPGAs, competing in a differentiated segment against market leaders AMD Xilinx and Intel Altera.

Lattice Q1 Results:

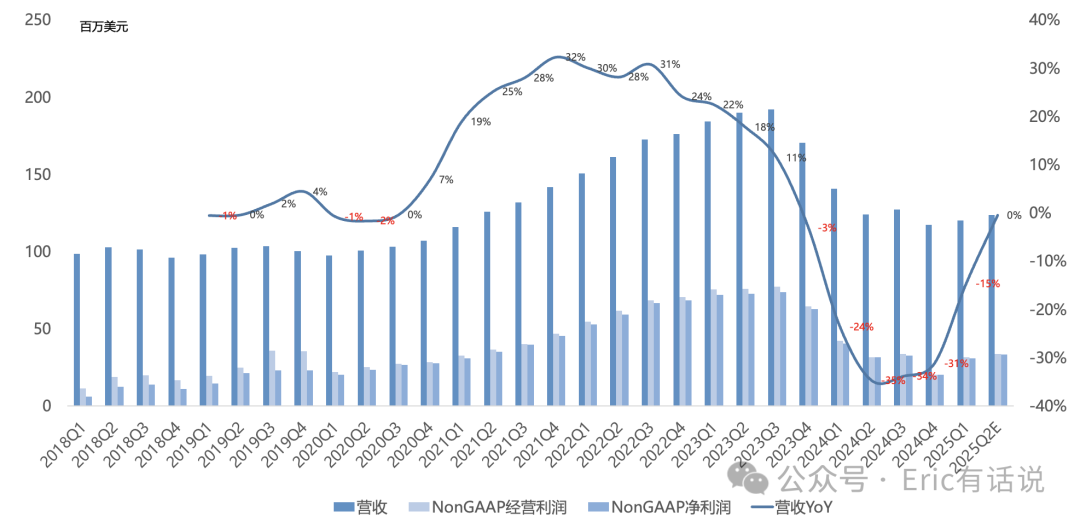

Revenue $120M, down 15% year over year, up 2% sequentially, marking the sixth consecutive quarter of year-over-year decline;

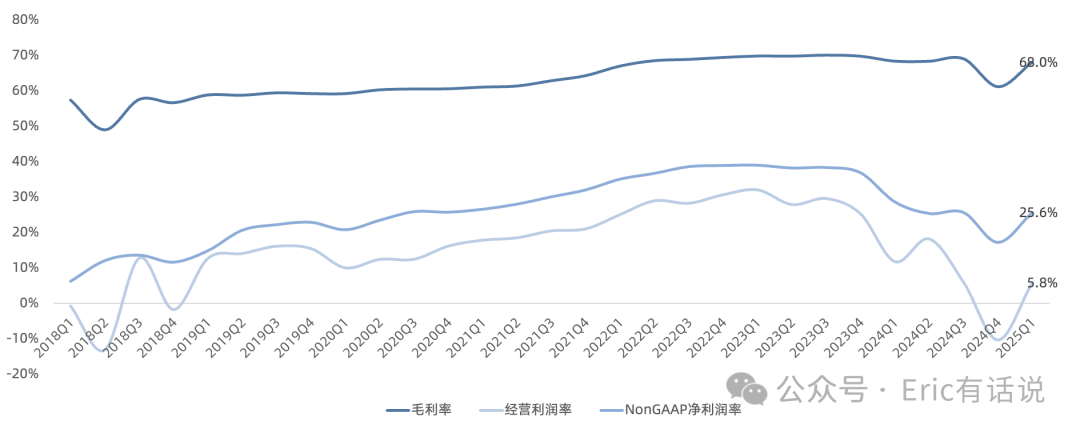

GAAP gross margin 68%, down 0.3 percentage points year over year, up 6.9 percentage points sequentially; operating income $7M, down 58% year over year, sequentially swinging from loss to profit;

Non-GAAP operating income $31.5M, down 25% year over year, up 57% sequentially, Non-GAAP operating margin 26.2%, down 3.8 percentage points year over year, up 9.1 percentage points sequentially;

Non-GAAP net income $30.7M, down 24% year over year, up 52% sequentially, Non-GAAP net margin 25.6%;

This quarter repurchased $25M, marking the 18th consecutive quarter of buybacks, with $75M remaining under the authorization;

No material impact from tariffs on results seen yet; will continue to monitor indirect effects;

Three demand improvement signals emerged this quarter: improving customer consumption, increasing backlog orders, and book-to-bill ratio remaining above 1;

One of Lattice's strengths is that its gross margin and net margin levels rank among the higher end in the semiconductor industry, which was the reason for continued coverage; it must be said that the FPGA track indeed has high margins, and even at the industry trough, gross margins can remain this high, which is truly remarkable.

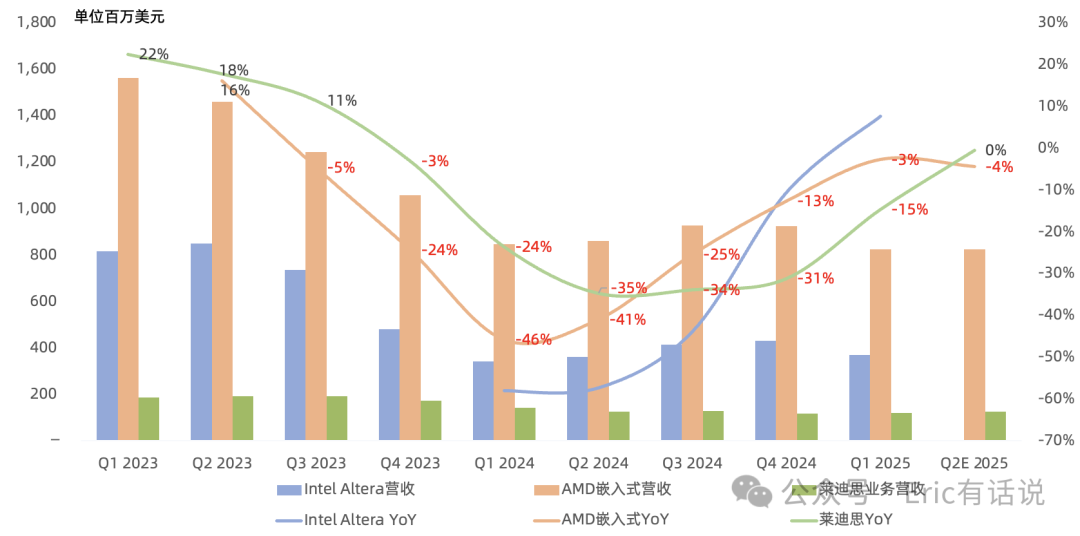

Since 2024, automotive semiconductors have continued to blow up, and Intel Altera and AMD Xilinx FPGA demand has been weak; Lattice cannot escape unscathed, and the entire FPGA market is in distress: AMD Embedded (mostly Xilinx) Q1 revenue $823M, down 3% year over year, the seventh consecutive quarter of year-over-year decline, yet operating margin remains as high as 40%; Intel Altera Q1 revenue $368M, up 8% year over year;

Q2 AMD Xilinx revenue guidance is flat sequentially, but Lattice guides for sequential growth, maintaining the 2025 industry U-shaped recovery expectation unchanged. AMD stated that embedded demand continues to recover gradually, book-to-bill continues to improve, and demand improvement in test, communications, and aerospace will drive a return to growth in H2 2025, while industrial remains weak, which is basically consistent with Lattice's guidance.

Q1 Segment Results:

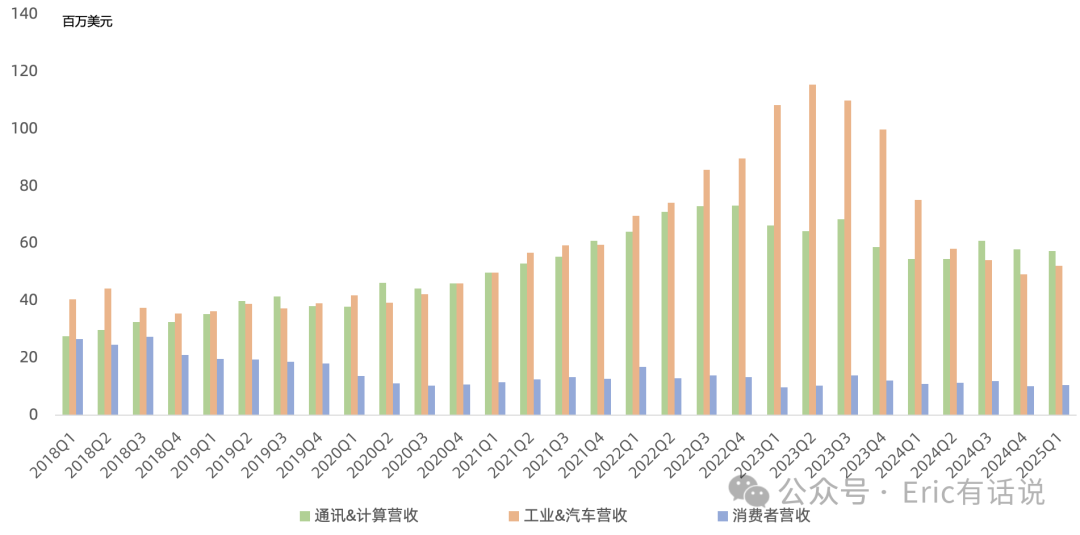

Industrial and automotive revenue $52.2M, down 31% year over year, but up 6% sequentially, first sequential increase in six quarters, accounting for 43% of revenue;

Communications and Compute revenue was $57.4M, up 5% year over year, ending seven consecutive quarters of decline, accounting for 48% of revenue; Compute growth was driven primarily by servers, while Communications growth was driven primarily by data center infrastructure.

Consumer revenue was $10.6M, down 3% year over year, accounting for 9% of revenue.

Products:

Lattice currently has three main business lines: two FPGA hardware platforms and one software development platform; management previously stated the software development platform generated quarterly revenue of a few million dollars, but has not updated the figure since;

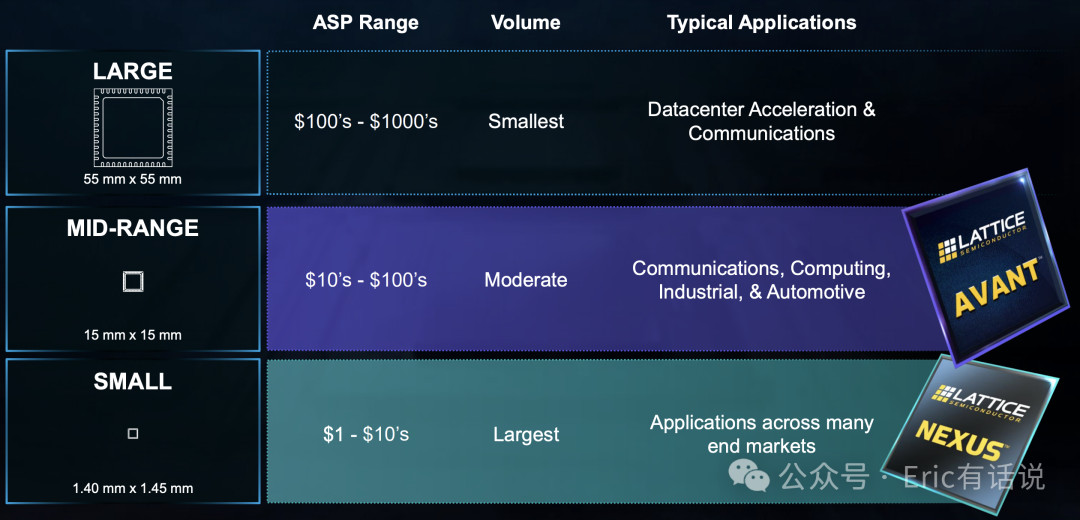

On the FPGA side, small FPGA products currently include 8 Nexus series models, with 1 Nexus 2 series model; last year's new Avant product line opened the mid-range FPGA market, with 3 series (E/G/X corresponding to edge/general-purpose/interconnect);

Q1 new product revenue achieved double-digit growth both year over year and sequentially; expecting 2025 new product revenue share in the high-teens%, 2026 share in the mid-20%s; Nexus products to accelerate growth in 2026, Avant products in 2027; design life 20-30 years; the characteristic of FPGAs and their products and applications is their very long lifespan;

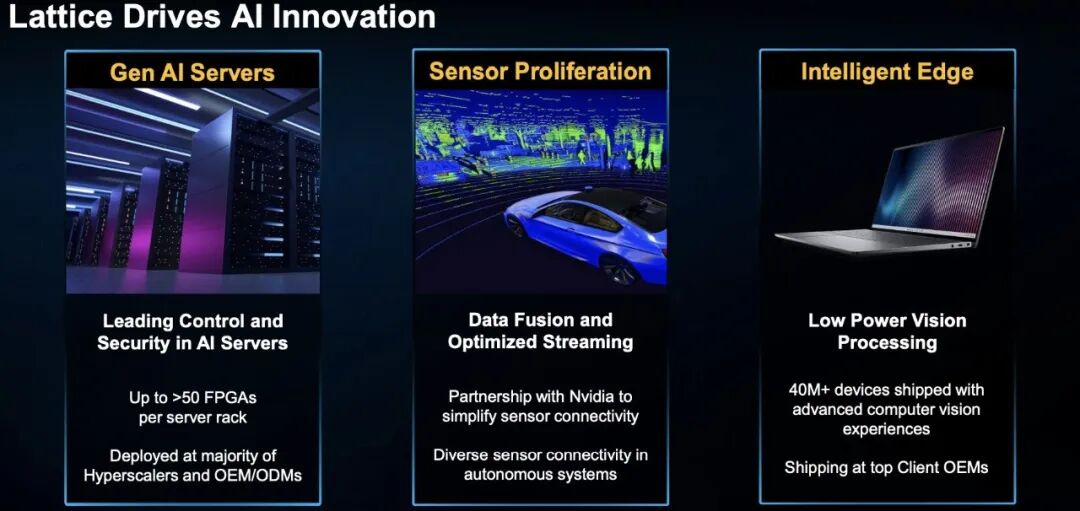

AI Exposure:

Existing product AI use cases: server control/security chips, AI PC detection chips, ADAS chips; management has still not disclosed the scale of AI exposure.

Currently seeing design wins continue to grow in emerging demand across generative AI and data centers, industrial robotics, automotive cockpit and ADAS, consumer AR/VR, and including quantum security.

Outlook:

Expecting Q2 revenue $119-129M, down 4% to up 4% year over year; Non-GAAP gross margin ~69%, Non-GAAP net income $30.43-35.96M, down 3% to up 14% year over year;

Remaining cautious on H2 outlook, expecting 2025 industry recovery to be U-shaped rather than V-shaped, company revenue low single-digit growth, net income double-digit growth (unchanged); expecting 2026 revenue up 15-20% year over year;

Small to mid-range FPGA design wins at a record high, multiple times revenue; company market share continues to rise; management noted that Xilinx and Altera currently use LUT-6 and more complex ALM architectures, while Lattice's products use LUT-4 architecture, which has certain advantages in the sub-million logic element range;

Company expects shipments below actual customer demand to persist in digesting inventory; previously expected industry inventory to normalize by mid-2025 (DIO 90), management now indicates a delay of several quarters;

Actual exposure within mainland China is far smaller than the disclosed shipments-to-China exposure; domestic Chinese FPGA vendors are relatively strong in communications and compute, while the company's China revenue is still growing, whereas Xilinx and Altera are declining;

Previously noted from a valuation perspective, due to Lattice's sustained high growth in prior years, its valuation has long remained elevated, making it difficult to initiate a position; this cycle downturn may instead present an opportunity, but the industry cycle recovery remains very long.

Based on a simple calculation from this earnings call, 2026 revenue roughly $600M, Non-GAAP net income optimistically $200M, current market cap implies ~34x PE. Meanwhile Intel recently sold Altera equity at a valuation of only $8.75B, which is not good news for Lattice.