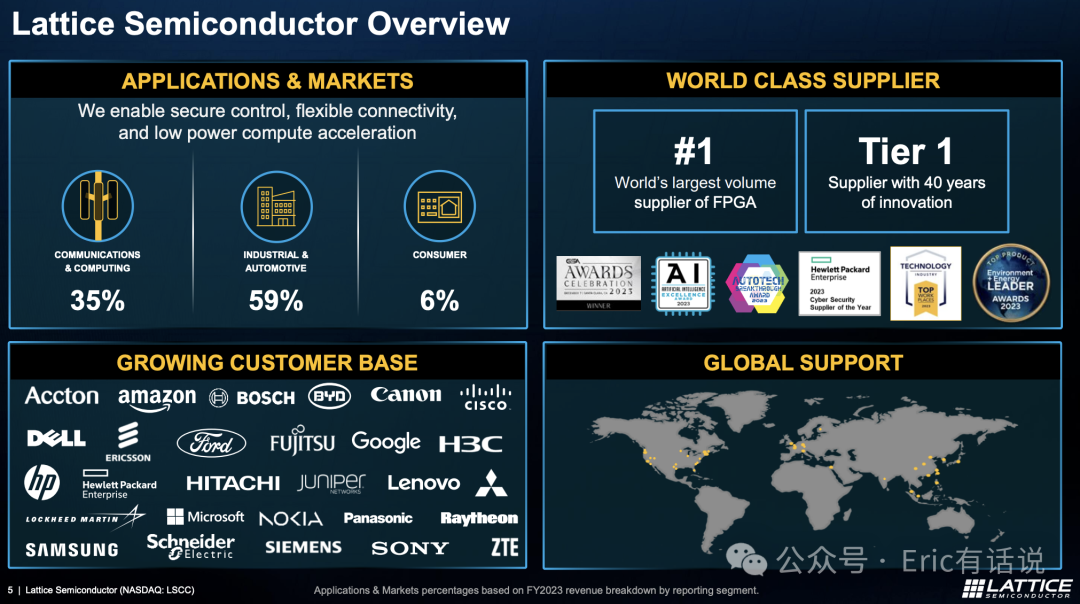

Lattice leads global shipments of low-power FPGAs, competing in a differentiated segment against market leaders AMD Xilinx and Intel Altera.

Lattice Q4 Earnings:

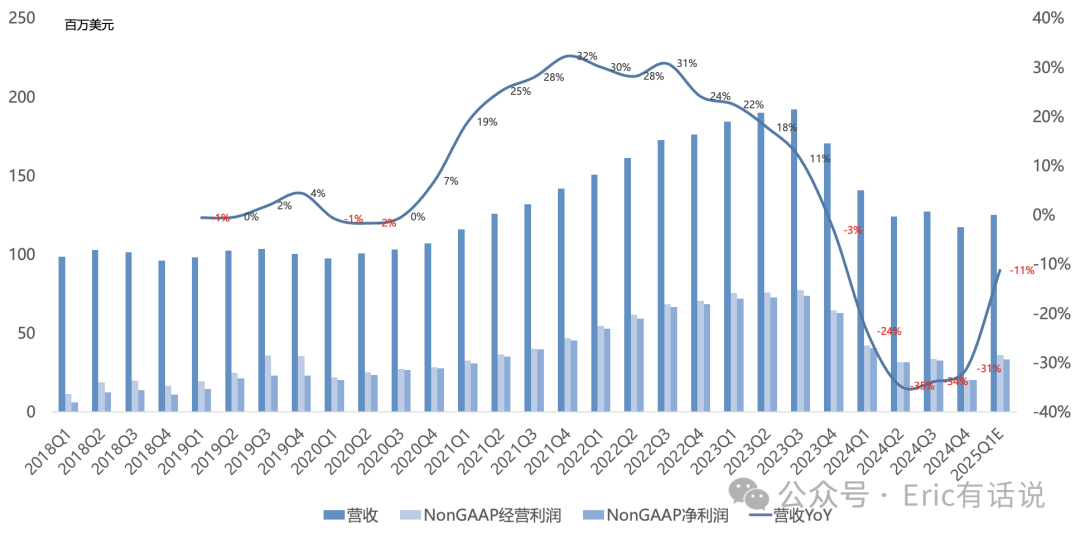

Revenue $117M, down 31% YoY, up 2% sequentially; fifth consecutive quarter of YoY decline; lowest since 2021Q1;

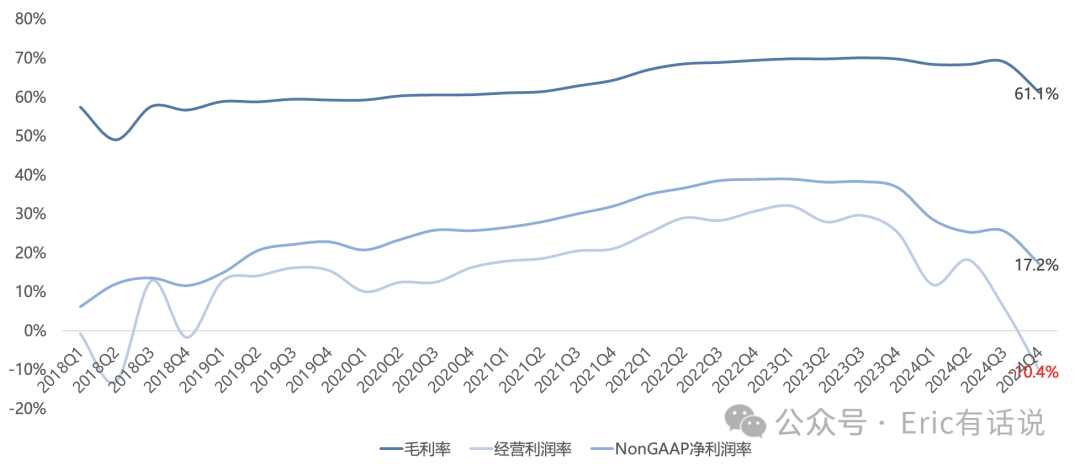

GAAP gross margin 61%, down 8.6pp YoY, down 7.9pp sequentially; operating loss $12.2M, first operating loss since 2018; Non-GAAP operating income $20.1M, down 69% YoY, Non-GAAP operating margin 17.1%, down 20.7pp YoY, down 9.5pp sequentially, lowest since 2018Q1;

Non-GAAP net income $20.2M, down 68% YoY, down 38% sequentially, back to 2019 levels; Non-GAAP net margin 17.2%;

$20M repurchased this quarter, 17th consecutive quarter of buybacks; announced additional $100M buyback authorization;

Executive changes: new CFO Lorenzo Flores, formerly Intel Foundry CFO, Kioxia Vice Chairman, Xilinx CFO; new CPO Nicole Singer, formerly SiFive CHRO, Synaptics CHRO, Xilinx HRD;

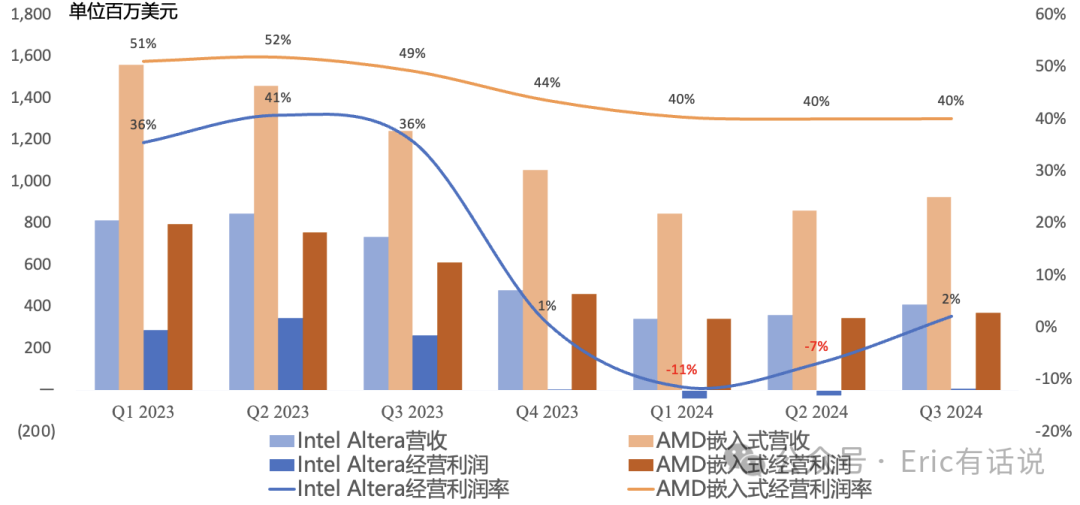

A Lattice strength is gross and net margin levels that rank near the top of semiconductors, which is why I've tracked it; FPGA lane margins are indeed high, and even at the cycle trough, gross margin holding this high is remarkable.

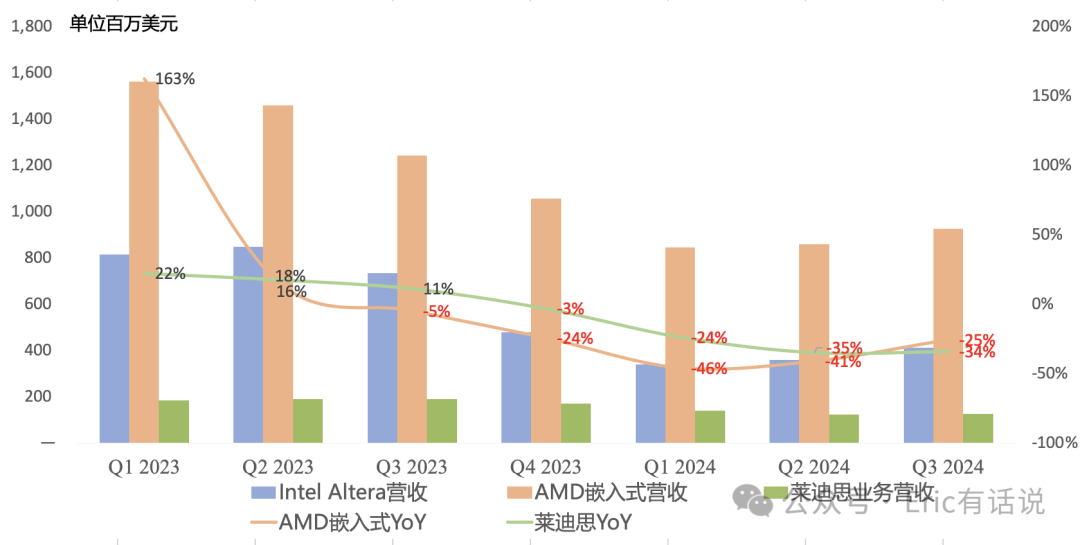

Since 2024, automotive semiconductors have continued to blow up, and demand for Intel Altera and AMD Xilinx FPGAs has been weak. Lattice has not been immune; the entire FPGA market is in distress: AMD Embedded (mostly Xilinx) Q4 revenue was $923M, down 13% year over year, with operating margin still at 39%; Intel Altera Q4 revenue was $429M, down 11% year over year, with operating margin of 21%.

Q1 AMD Xilinx and Intel Altera revenue guides both down sequentially, but Lattice guides up sequentially; maintaining 2025 industry U-shaped recovery view unchanged.

By Segment Q4:

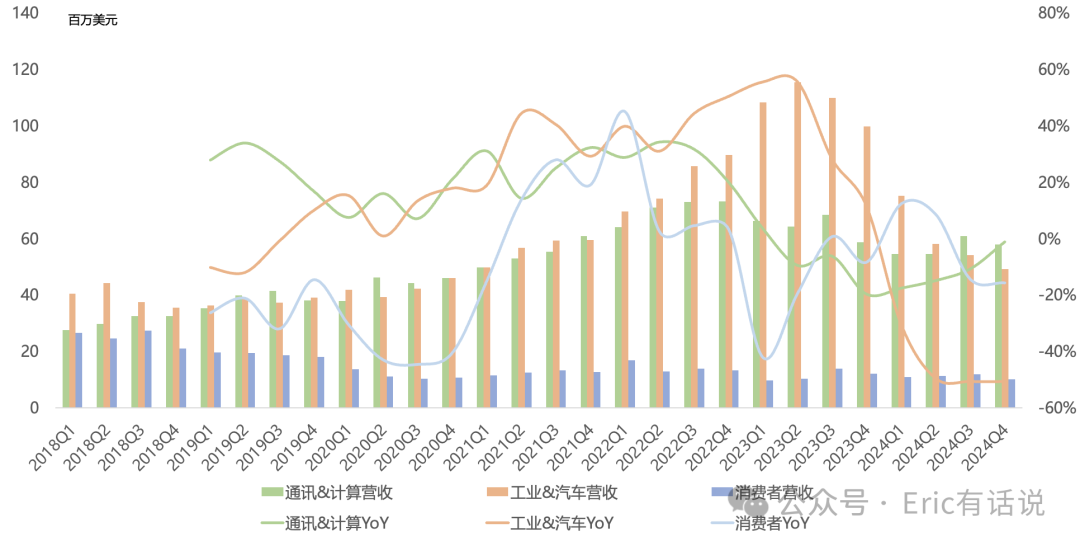

Industrial and auto revenue $49.2M, down 51% YoY, revenue share 42%; industrial and auto is Lattice's highest-margin business; auto recovered more sequentially; industrial and auto in early recovery; expect continued improvement in 2025, H2 demand > H1;

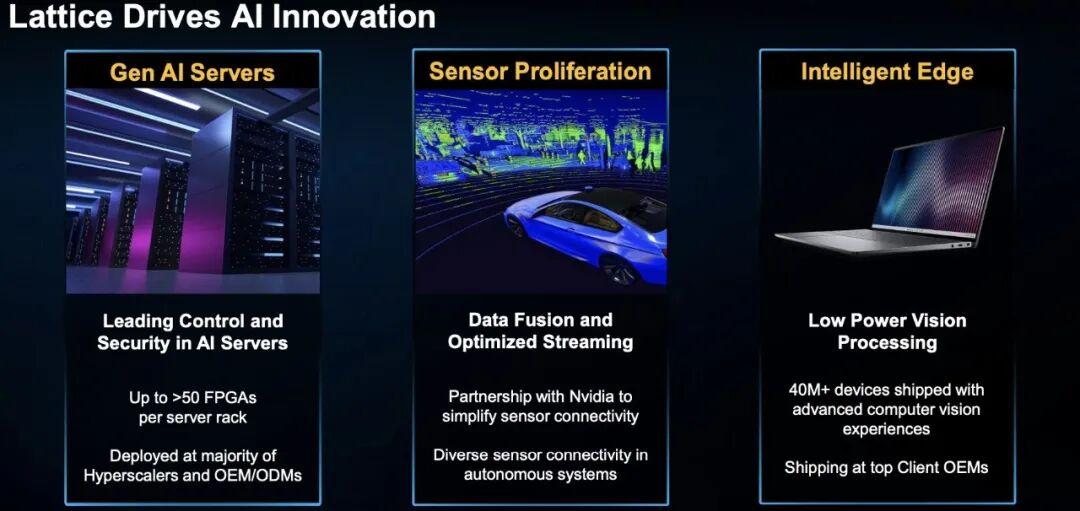

Communications and compute revenue $58M, down 1% YoY, seventh consecutive quarter of decline, revenue share 49%; full-year compute revenue up YoY, server revenue double-digit growth, 2025 demand remains strong; one OEM server customer using >50 FPGAs per rack; wireless communications remains weak, 5G industry sentiment very low;

Consumer revenue $10.2M, down 16% YoY, revenue share 9%;

Products:

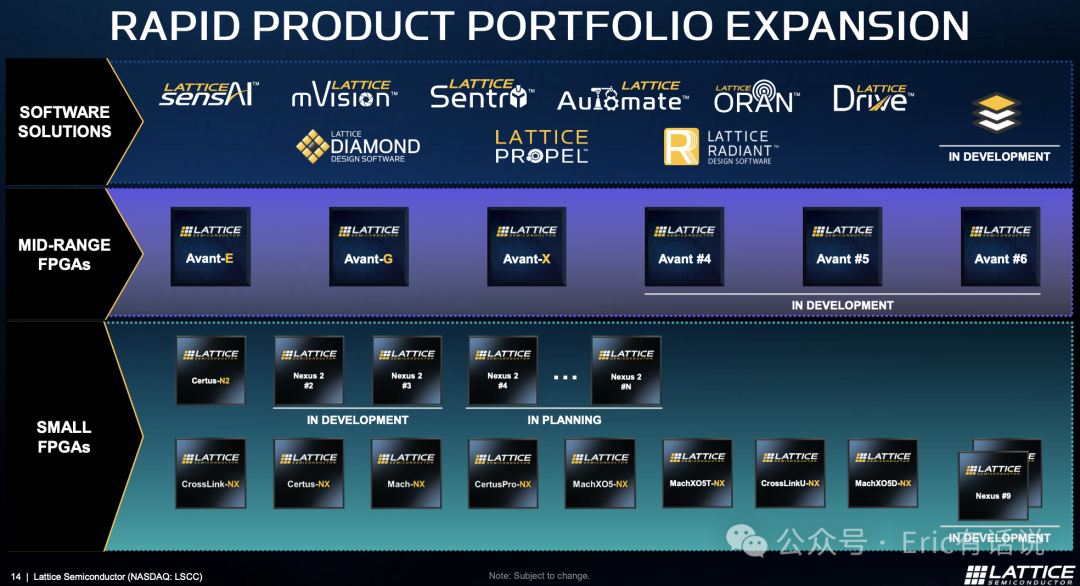

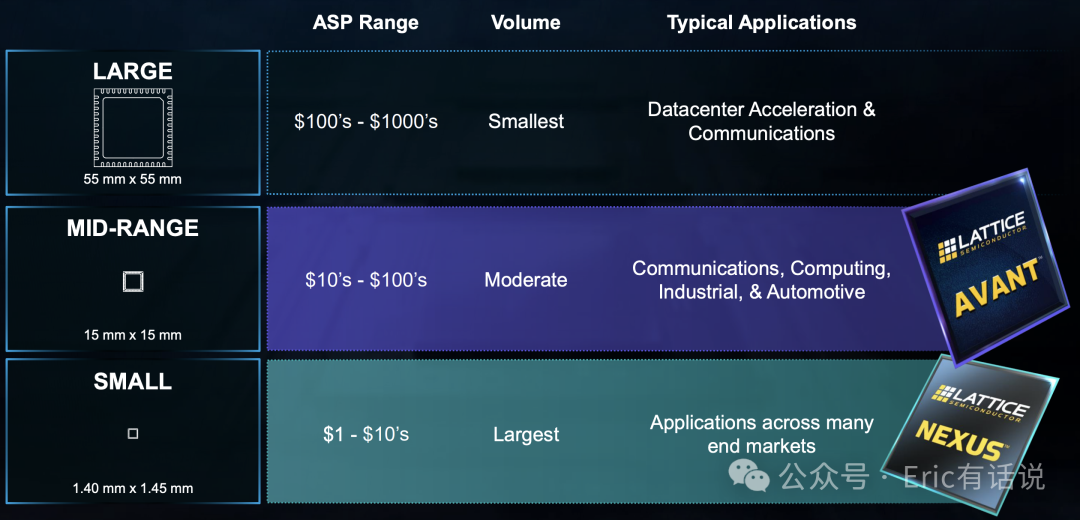

Lattice currently has three main business lines: two FPGA hardware platforms and one software development platform; management previously stated the software development platform generated quarterly revenue of a few million dollars, but has not updated the figure since;

FPGA side: small FPGA product launch Nexus 2 series; Nexus family now 8 parts, Nexus 2 series has 1 part;

Last year's new Avant product line opened the mid-range FPGA market, 3 series (E/G/X for edge/general/connectivity); 2024 new-product revenue up double-digits YoY; this quarter Avant/Nexus revenue share rose from single-digits a year ago to mid-teens% (>13%);

AI Exposure:

Current product AI use cases: server control/security chips, AI PC detection chips, ADAS chips; management still not disclosing AI exposure scale;

Outlook:

Guiding Q1 revenue $115-125M, down 11%-18% YoY; Non-GAAP gross margin ~69%; Non-GAAP net income $27.7-33.2M, down 18%-31% YoY;

Expect 2025 industry U-shaped not V-shaped recovery; company revenue low-single-digit growth, net income double-digit growth;

Small to mid-range FPGA market growing faster than other FPGA segments; company share rising; see large FPGA market as challenging;

Company expects shipments below actual customer demand to persist through mid-2025, working through inventory; 2025 mid-year industry inventory normalizes (DIO 90);

A few weeks ago book-to-bill ratio exceeded 1, first time in 6 quarters;

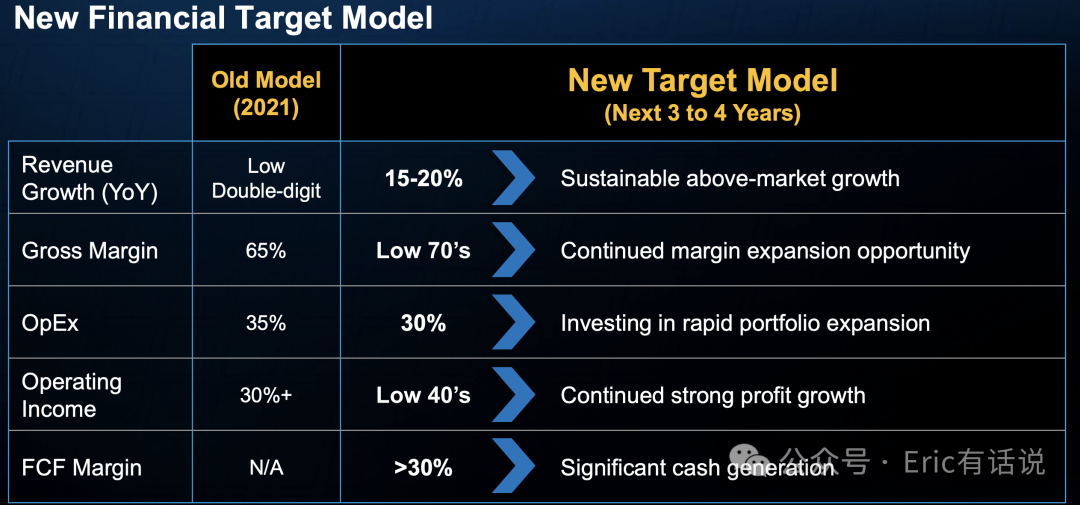

Long-term revenue CAGR target 15%-20% unchanged; expect to achieve by 2026;

Company not pursuing cloud data center FPGAs; believes FPGAs more flexible, efficient, lower cost than ASICs (Avant 16nm, Nexus 28nm);

Previously noted on valuation: Lattice's multi-year high growth kept valuation elevated, hard to enter; this downcycle may create opportunity, but industry recovery remains long. Interconnect chip upstart ALAB becoming a $10B+ 'darling', while former FPGA star fades into a 'value trap'.