Lattice leads global shipments of low-power FPGAs, competing in a differentiated segment against market leaders AMD Xilinx and Intel Altera.

Lattice Q2 Earnings:

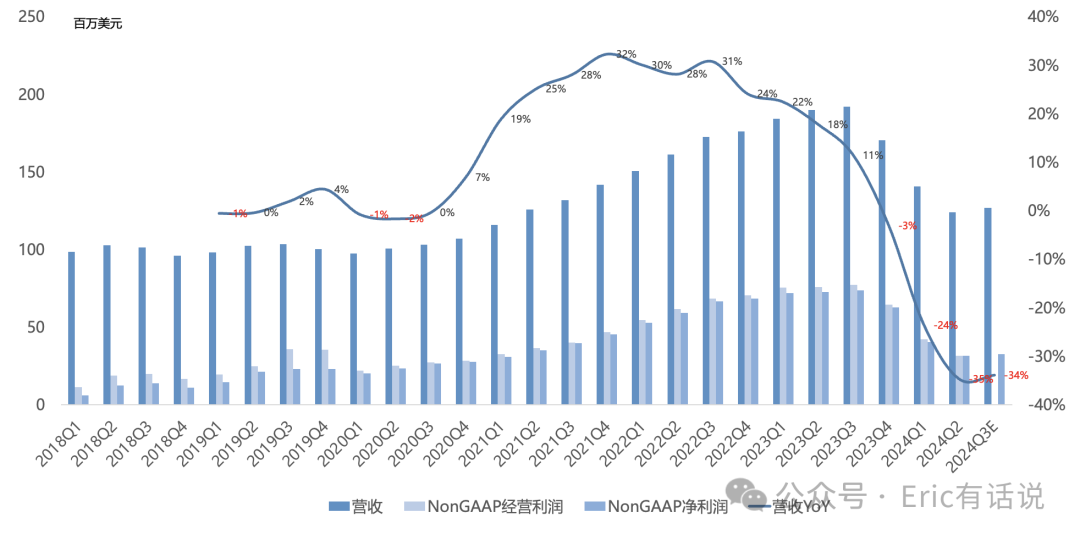

Revenue $124M, down 35% year over year and 12% sequentially. First time since 2020 with 3 consecutive quarters of year-over-year declines; first Q2 earnings miss.

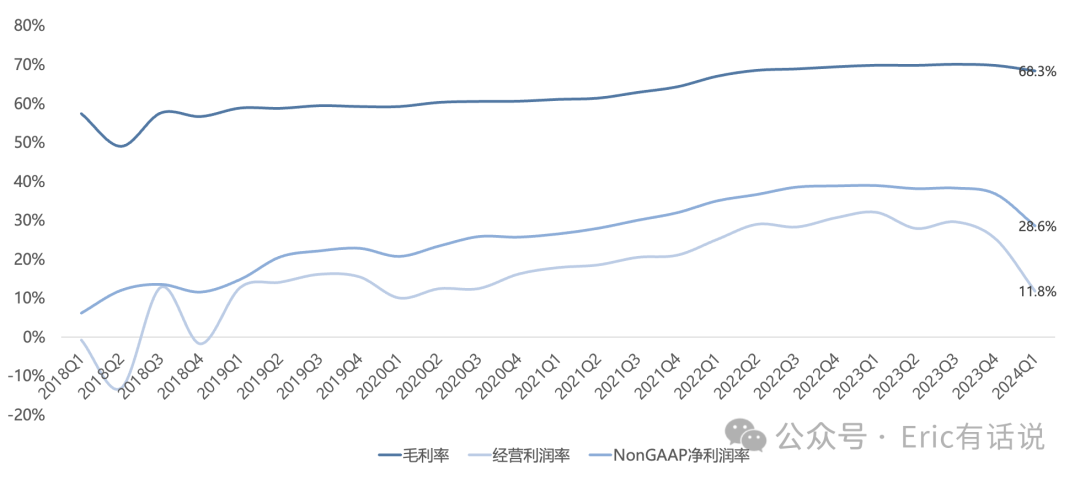

GAAP gross margin 68.3%, still at historical highs. Operating margin 18.2%, down 9.7 percentage points year over year, up 6.4 percentage points sequentially.

Non-GAAP net income $31.4M, down 57% year over year and 22% sequentially, back to 2021 levels. Non-GAAP net margin 25.3%, lowest since 2020 Q2.

$10M in share repurchases this quarter; 15th consecutive quarter of buybacks.

A Lattice strength is gross and net margin levels that rank near the top of semiconductors, which is why I've tracked it; FPGA lane margins are indeed high, and even at the cycle trough, gross margin holding this high is remarkable.

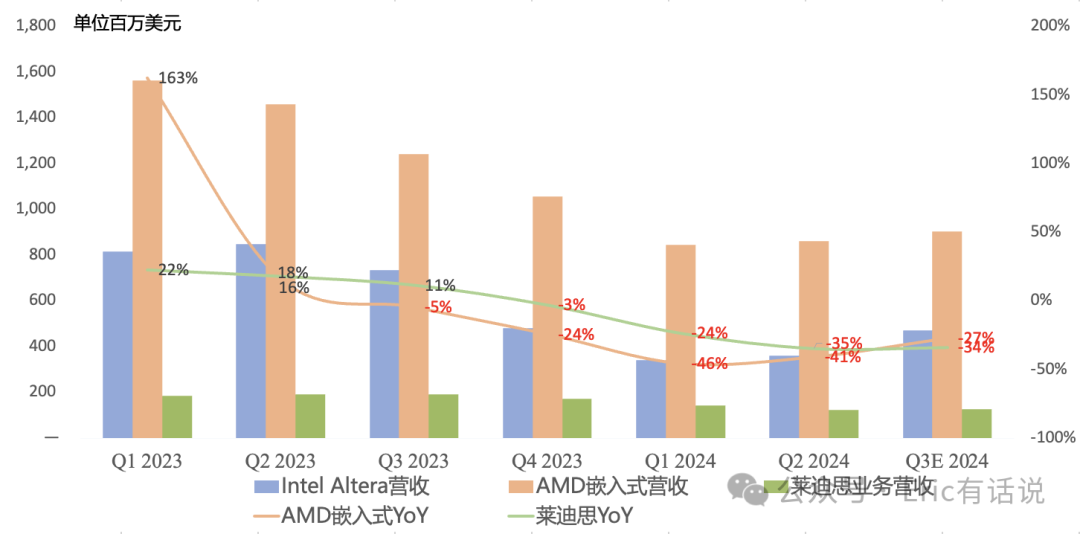

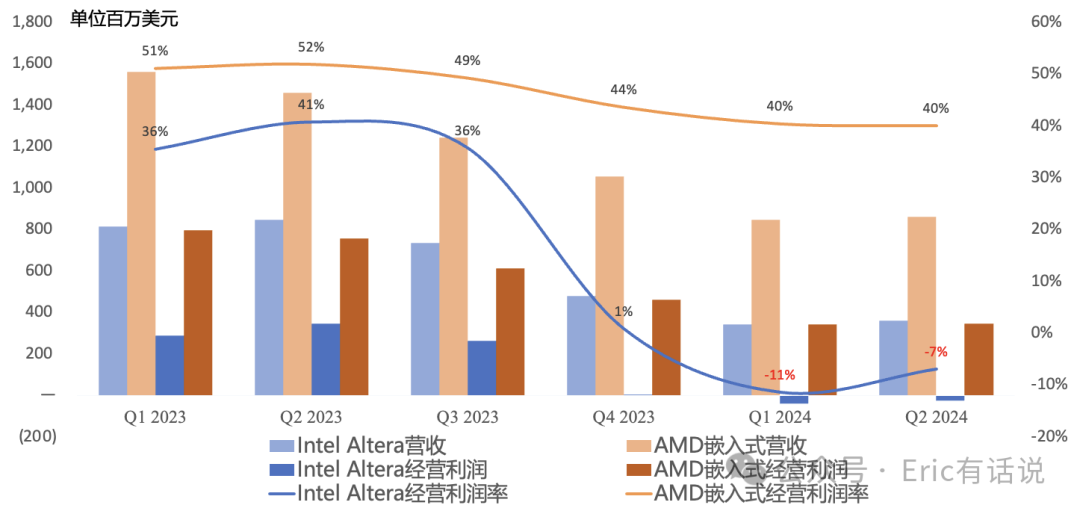

At the start of 2024, automotive semiconductors blew up one after another, while Intel Altera and AMD Xilinx saw weak FPGA demand. Lattice could not remain unscathed, and the entire FPGA market was in distress: AMD Embedded (mostly Xilinx) Q2 revenue was $861M, down 41% year over year, with operating margin still as high as 40%, which is remarkable; Intel Altera Q2 revenue was $361M, down 57% year over year, posting an operating loss for the second consecutive quarter.

However, per management guidance, AMD Xilinx and Intel Altera both guided to sequential revenue growth in Q3, expecting customer orders to recover in the second half.

Q2 by Segment:

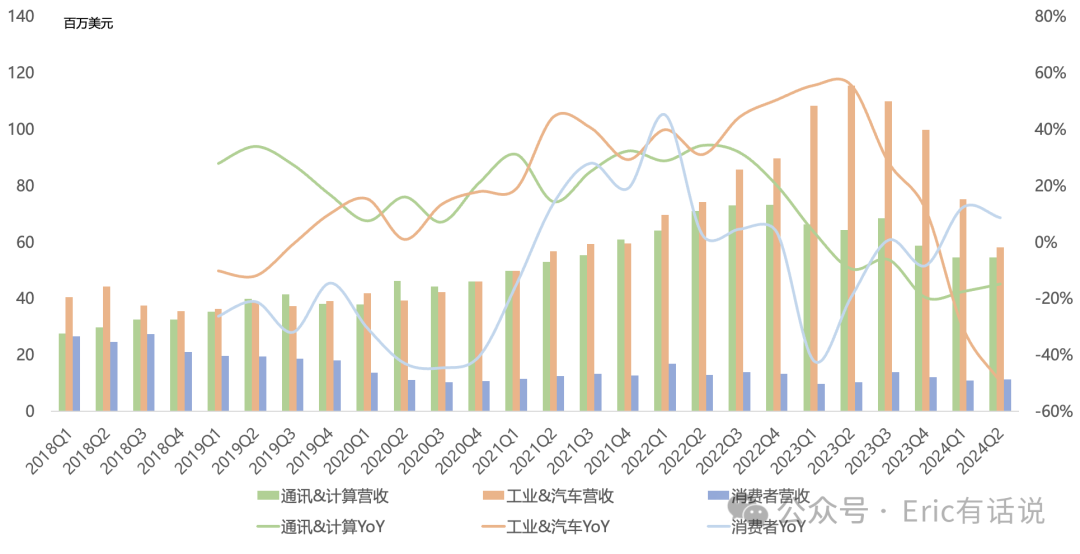

Industrial and automotive revenue $58.2M, down 50% year over year, 47% of revenue. This is Lattice's highest-margin business. Industrial and auto demand weaker than expected; customers continue destocking. Industrial market still has growth pockets in robotics and factory automation.

Communications and compute revenue $54.6M, down 15% year over year, 5th consecutive quarterly decline, 44% of revenue. Compute revenue up sequentially, driven by strong data center networking and server demand; storage applications also exceeded expectations. 5G demand in communications very weak; industry sentiment very low. Compute revenue now far exceeds communications revenue.

Consumer revenue $11.3M, up 9% year over year, 9% of revenue.

Products:

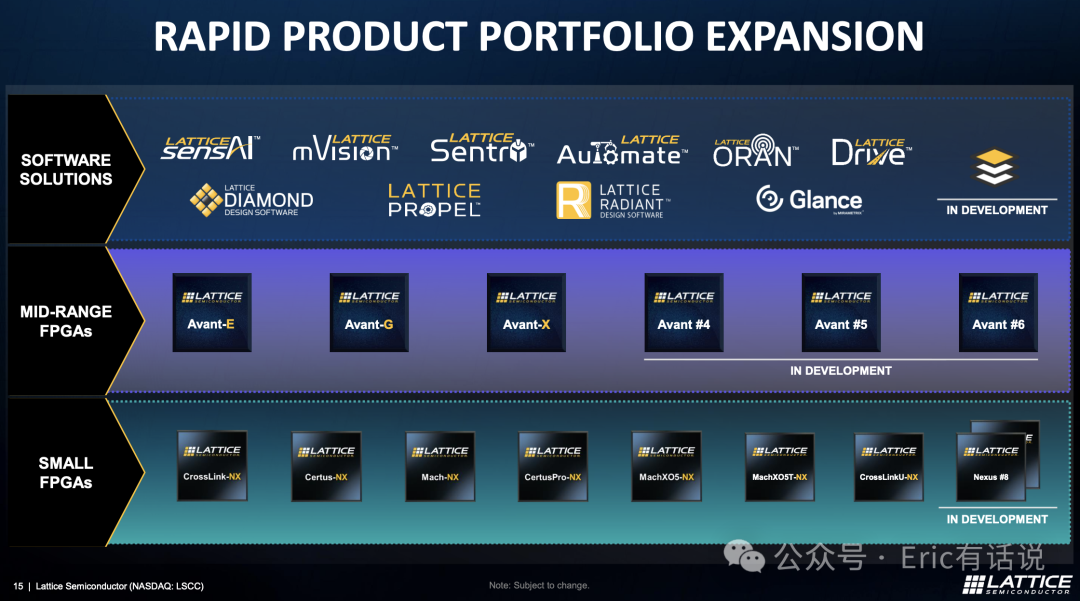

Lattice has three main business lines: two FPGA hardware lines and one software development platform; management previously said software platform quarterly revenue was a few million dollars, but has not updated the figure since.

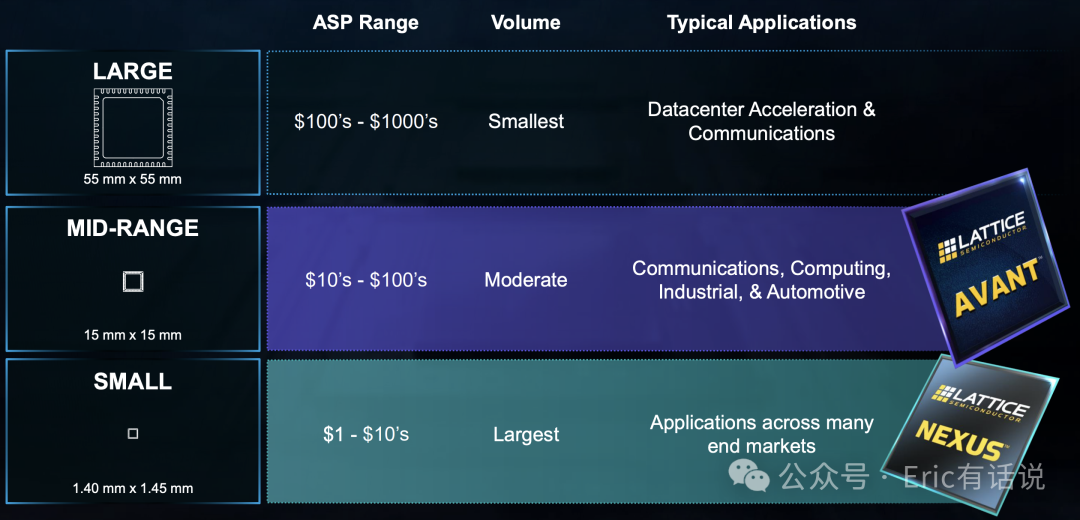

FPGA side: small FPGA Nexus family has 7 products; 6 in volume production, 7th ramping on track in Q3. Nexus remains the primary shipment driver in 2024.

Last year's new Avant product line opened the mid-range FPGA market, with 3 series (E/G/X for edge/general/connectivity). G/X series launched December last year; revenue contribution starting late this year. Over the next 2-3 years, Avant expected to reach 10-15% of company revenue. Avant E began contributing revenue late last year; ramping in H2 this year. H1 Nexus and Avant revenue already exceeded year-ago levels (implying pre-Nexus products declined sharply; management says Nexus demand stable).

AI Exposure:

Current product AI use cases: server control/security chips, AI PC detection chips, ADAS chips; management still not disclosing AI exposure scale;

Outlook:

Q3 revenue guided at $117-137M, down 29-39% year over year. Non-GAAP gross margin ~69%. Non-GAAP net income ~$25.7-39.5M.

Product pricing firm. Bookings recovered in Q2; Q3 backlog expected to grow sequentially. Last quarter guided H2 revenue better than H1; this quarter management declined to commit, saying to wait for Q3 earnings.

Expect to ship below actual customer demand for 3 consecutive quarters, working through inventory.

Xilinx exiting low-end FPGA market benefits Lattice.

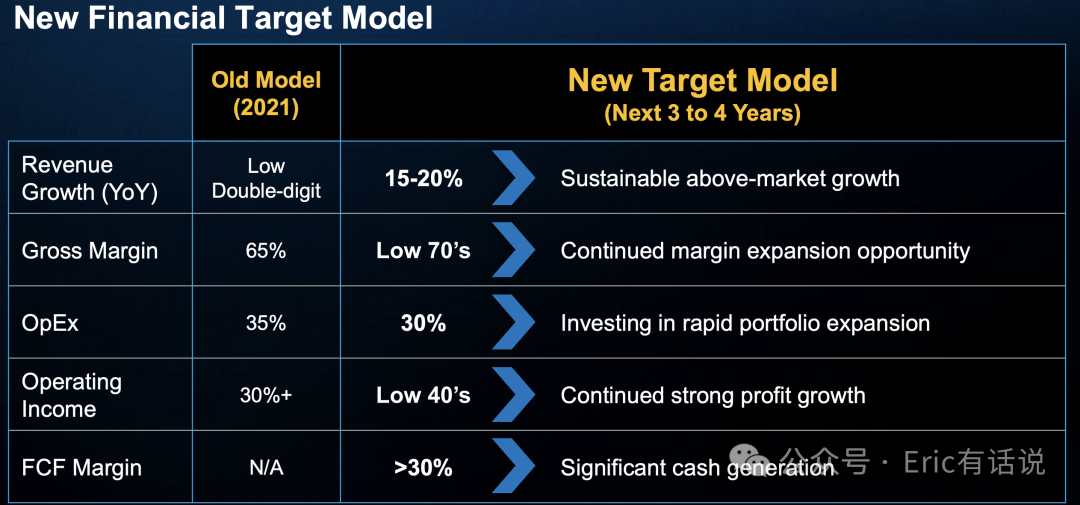

Maintain 2022-2026 revenue CAGR target of 15-20%.

Previously noted on valuation: Lattice's sustained high growth in prior years kept valuations elevated for a long time, making entry difficult. The current downcycle may present an opportunity.

FPGA Tier 1 players Xilinx and Altera both guided H1 bottom, weak H2 recovery. Given Lattice's persistent guidance cuts, its profits may not have bottomed even in H1.

Long term, Avant can indeed open Lattice's second growth curve, but a near-term bottom and rebound will take time.