Lattice leads global shipments of low-power FPGAs, competing in a differentiated segment against market leaders AMD Xilinx and Intel Altera.

Lattice Q3 Earnings:

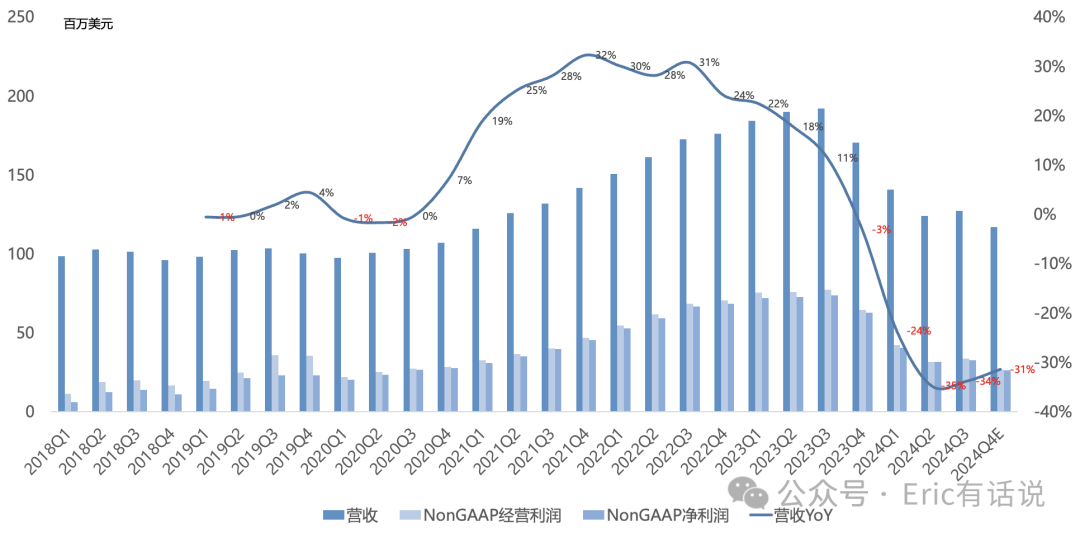

Revenue $127M, down 34% year over year, up 2% sequentially; fourth consecutive quarter of year-over-year decline.

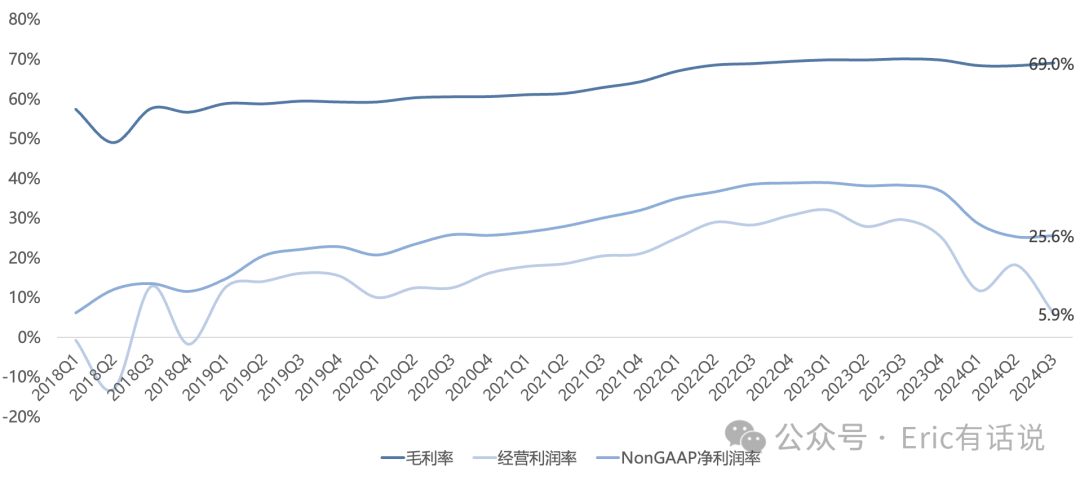

GAAP gross margin 69%, still near historical highs; operating margin 5.9%, down 23.7 percentage points year over year, mainly due to 14% headcount reduction causing a $6.5M one-time charge, Lattice's first large-scale layoff; operating cash flow doubled sequentially; Non-GAAP operating margin 26.6%, down 13.7 percentage points year over year.

Non-GAAP net income $32.5M, down 56% year over year, up 4% sequentially, back to 2021 levels; Non-GAAP net margin 25.6%.

Repurchased $17M this quarter, 16th consecutive quarter of buybacks.

Former CEO Jim Anderson was poached to become CEO of optical module giant Coherent; new CEO Ford Tamer spent 9 years as CEO of Inphi (later acquired by Marvell).

A Lattice strength is gross and net margin levels that rank near the top of semiconductors, which is why I've tracked it; FPGA lane margins are indeed high, and even at the cycle trough, gross margin holding this high is remarkable.

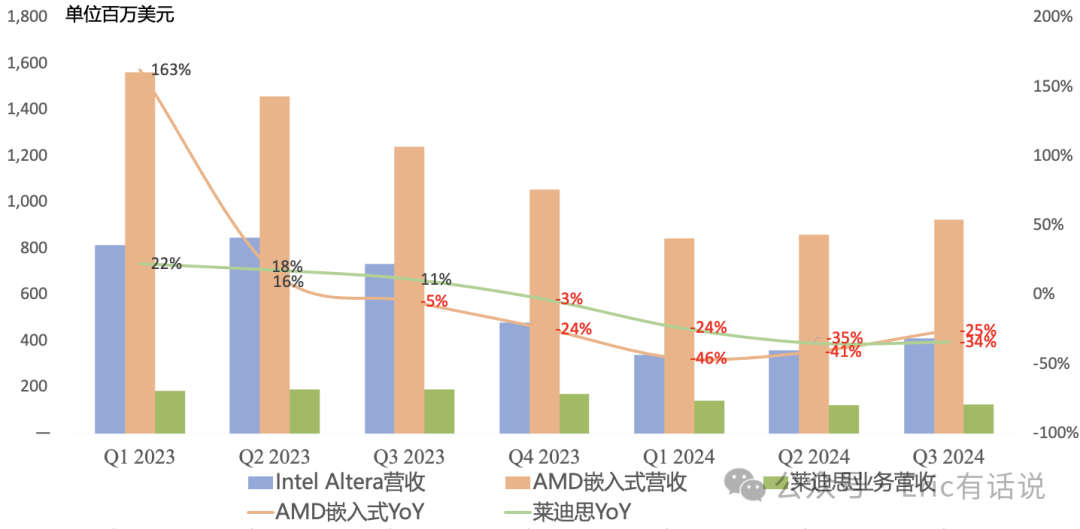

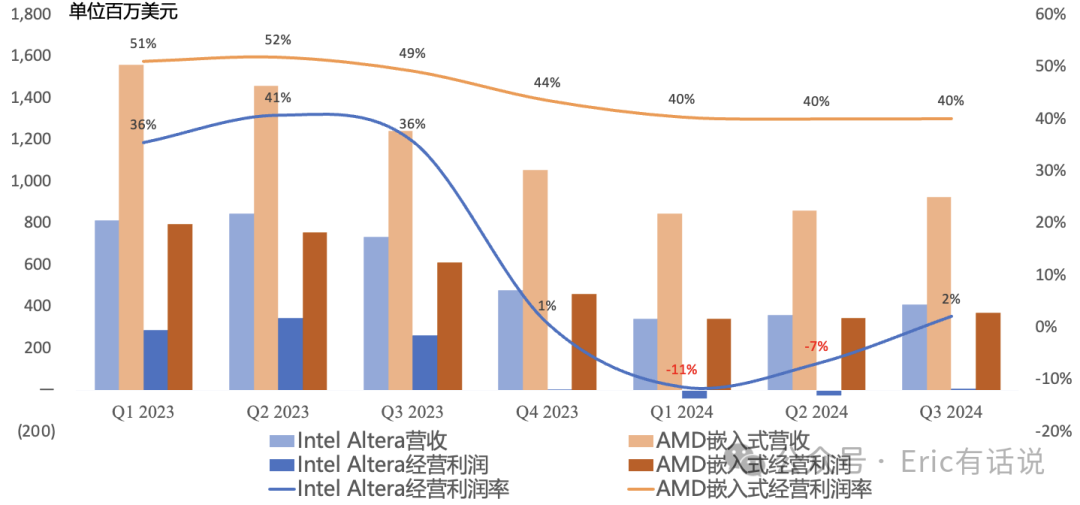

Since 2024, automotive semiconductors have continued to blow up, while Intel Altera and AMD Xilinx have seen weak FPGA demand. Lattice has been unable to stay unscathed, and the entire FPGA market is in distress: AMD Embedded (mostly Xilinx) Q3 revenue was $927M, down 25% year over year, with operating margin still as high as 40%; Intel Altera Q3 revenue was $412M, down 44% year over year, with operating margin of 2%.

Although Q4 guidance for both AMD Xilinx and Intel Altera shows continued sequential growth, Lattice management is more cautious, expecting a U-shaped industry recovery in 2025.

Q3 by Segment:

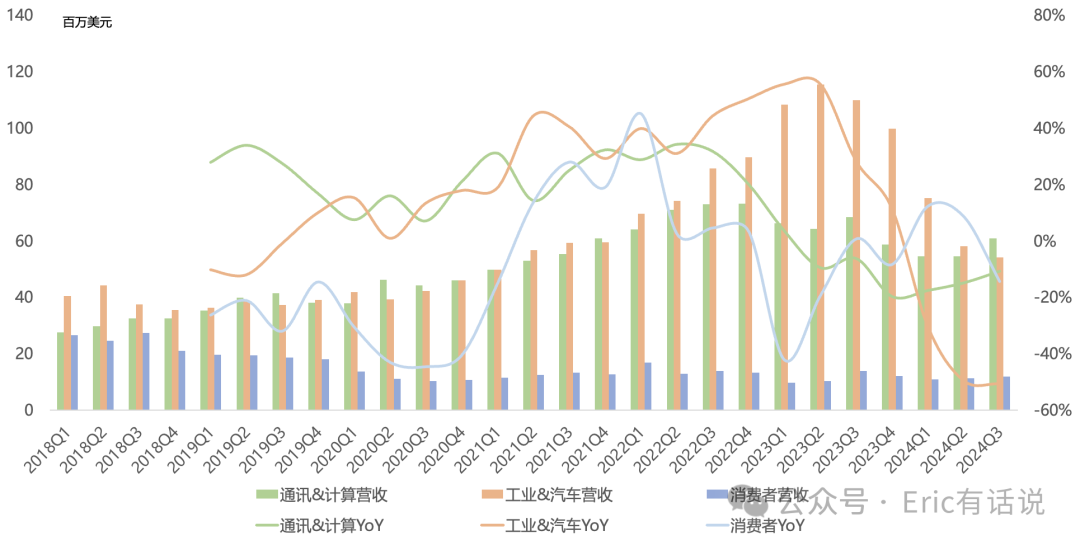

Industrial and automotive revenue $54.2M, down 51% year over year, 43% of revenue; industrial and automotive is Lattice's highest-margin business; industrial and auto demand remain weak, customers continue destocking; 5 of top 6 automotive LiDAR vendors use company FPGAs.

Communications and compute revenue $61M, down 11% year over year, sixth consecutive quarterly decline, 48% of revenue; compute revenue continues to grow sequentially, driven by server demand; one OEM server customer uses 50+ company FPGAs per server, expect strong 2025 demand; wireless communications remains weak, 5G industry sentiment very low.

Consumer revenue $11.9M, down 14% year over year, 9% of revenue.

Products:

Lattice has three main business lines: two FPGA hardware lines and one software development platform; management previously said software platform quarterly revenue was a few million dollars, but has not updated the figure since.

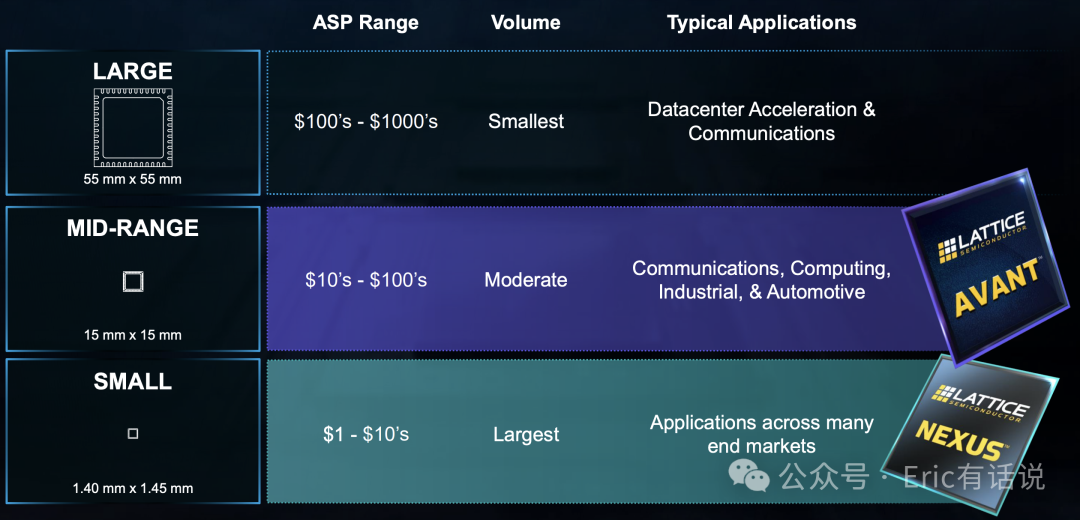

On FPGA side, small FPGA Nexus series has 8 products, 7th product in volume production in Q3.

Last year's new Avant product line opened the mid-range FPGA market, with 3 series (E/G/X for edge/general-purpose/connectivity); G/X series launched Dec last year, started contributing revenue in Q4; Avant E series started contributing revenue late last year, ramped in H2 this year.

AI Exposure:

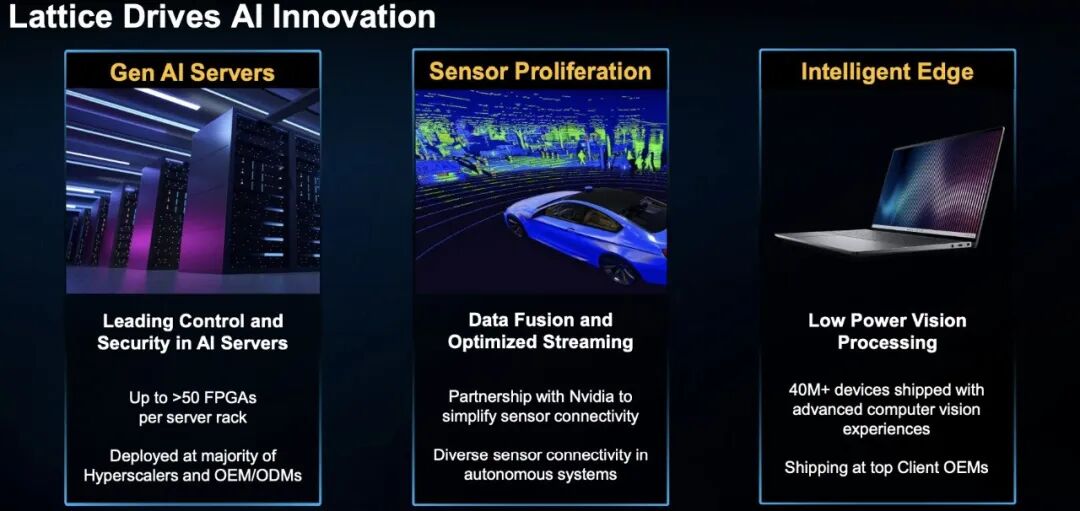

Current product AI use cases: server control/security chips, AI PC detection chips, ADAS chips; management still hasn't disclosed AI exposure size but says AI revenue share continues to rise.

Outlook:

Expect Q4 revenue $112M-$122M, down 29%-34% year over year; Non-GAAP gross margin ~68%; Non-GAAP net income $20.7M-$31.7M, down 50%-67% year over year.

Expect 2025 industry recovery to be U-shaped not V-shaped; company revenue low single-digit growth, opex down 14%, net income low double-digit growth; 2025 Q2/Q3 industry inventory to normalize (DIO 60-90).

Company market share in small to mid-range FPGA without SoC continues to rise.

Company expects shipments below actual customer demand to persist until mid-2025, working through inventory.

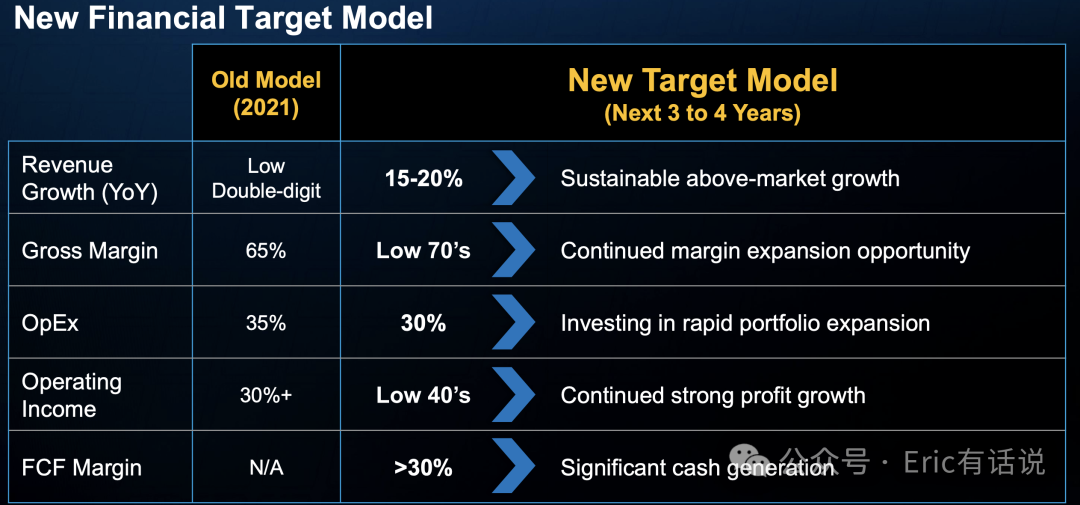

Long-term revenue CAGR target 15%-20% unchanged; expect to achieve by 2026;

Previously noted from a valuation perspective, due to Lattice's sustained high growth in prior years, its valuation has long remained elevated, making it difficult to initiate a position; this cycle downturn may instead present an opportunity, but the industry cycle recovery remains very long.

Intel Altera, expected to IPO next year, reportedly recently raised strategic capital at a $17B valuation; Intel paid $16.7B to acquire Altera in 2015. Another $10B+ giant, Astera, is becoming a towering tree.