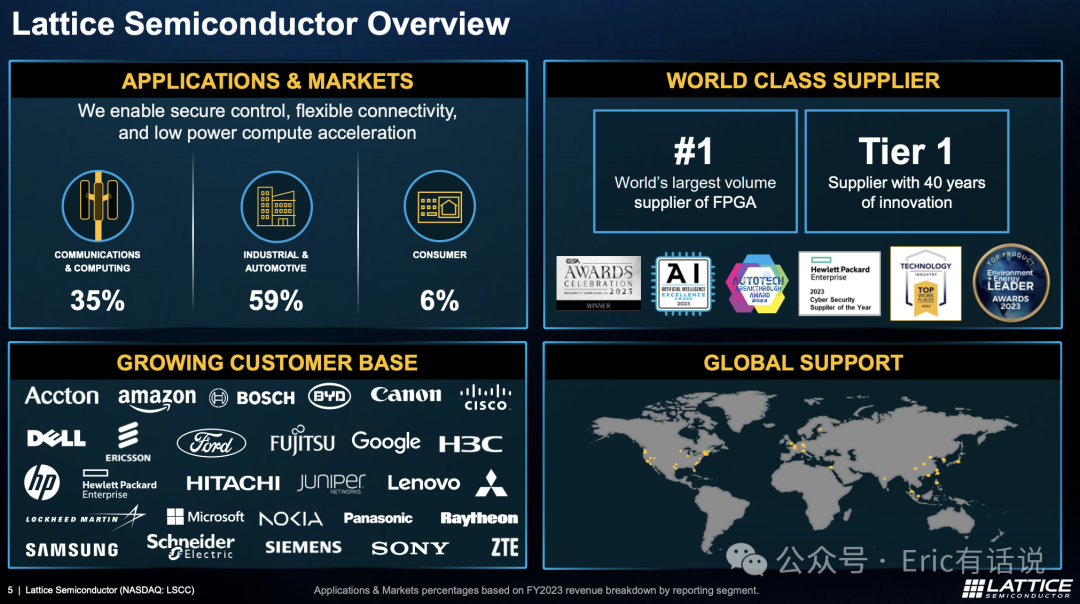

Lattice leads global shipments of low-power FPGAs, competing in a differentiated segment against market leaders AMD Xilinx and Intel Altera.

Lattice Q4 Earnings:

Revenue was $171M, down 3% year over year and 11% sequentially; first year-over-year decline since Q4 2020.

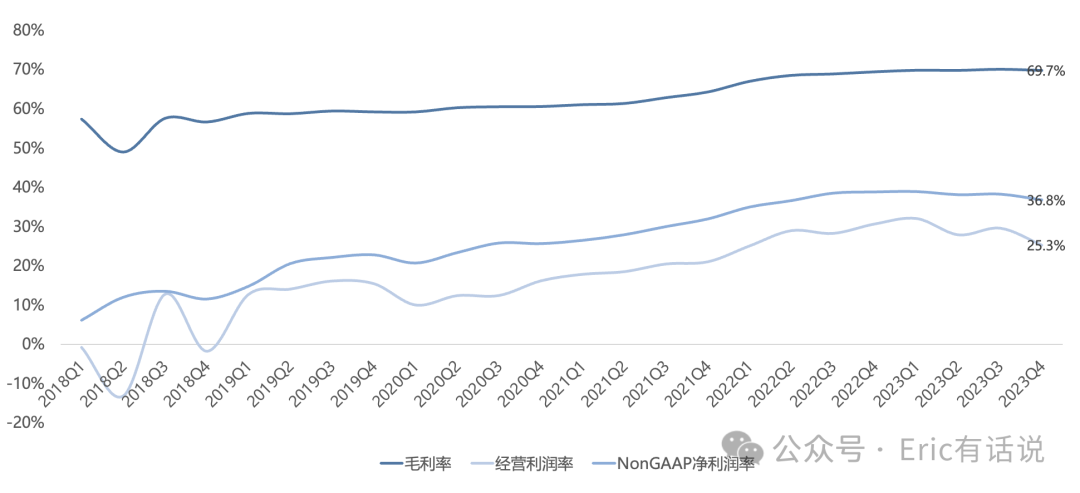

GAAP gross margin was 69.7%, operating margin 25.3%; though down sequentially, both remain at historical highs.

Non-GAAP net income was $62.8M, down 8% year over year and 17% sequentially; first year-over-year decline since Q1 2021; Non-GAAP net margin was 36.8%.

Approved a $250M share repurchase program; cumulative repurchases of 4.8M shares over the past 13 quarters.

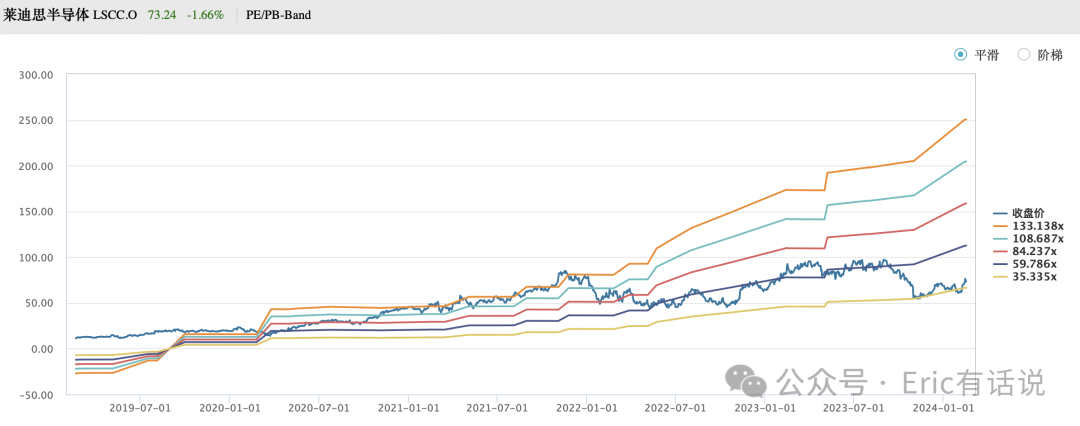

A key Lattice strength is that its gross and net margins rank among the highest in the semiconductor industry, which is why I have continued to follow it; the FPGA segment indeed commands high profitability.

However, the chart below makes clear that Lattice's fundamentals have deteriorated. Early 2024 blow-ups across automotive semiconductors, along with weak demand at Intel Altera and AMD Xilinx FPGA, all signal that Lattice is entering a downcycle.

By Segment Q4:

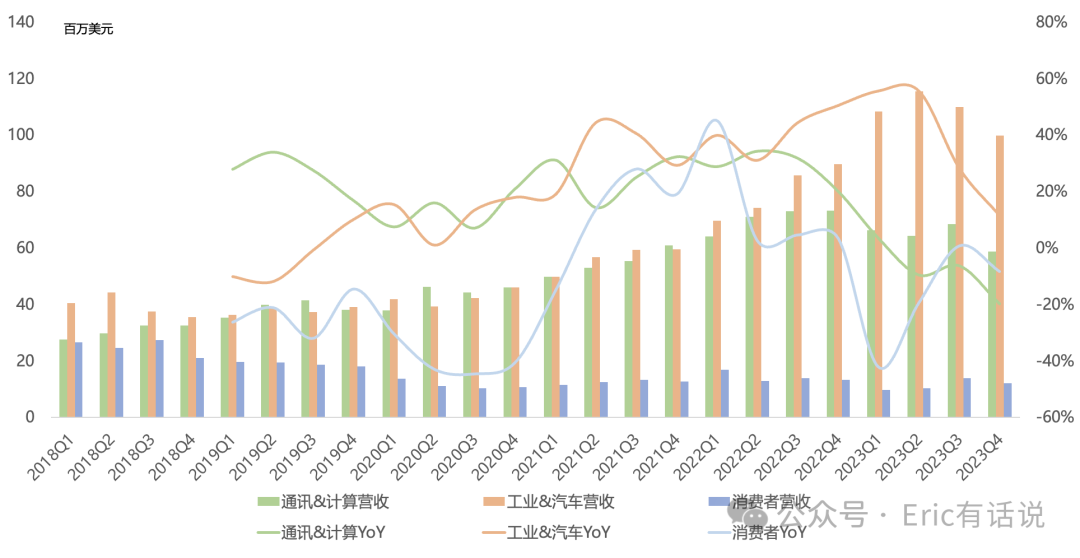

Industrial and automotive revenue was $99.8M, up 11% year over year, accounting for 59% of revenue; this segment carries Lattice's highest gross margins; due to macro headwinds, industrial and automotive demand is weak, customers continue to destock, and Q1 industrial and automotive revenue is expected to decline sequentially by more than in Q4.

Communications and compute revenue was $58.7M, down 20% year over year, marking the third consecutive quarterly decline, accounting for 34% of revenue; data center demand is strong with related revenue growing sequentially; wired/wireless telecom demand remains weak with revenue declining sequentially; compute revenue now exceeds communications; on next-generation server platforms, per-server content is growing 50%+.

Consumer revenue was $12.1M, down 8% year over year, accounting for 7% of revenue; Apple Vision Pro uses the company's single-chip iCE Ultra FPGA, priced at only a few dollars; management cited confidentiality and did not elaborate.

Products:

Lattice currently has three main product lines: two FPGA hardware families and a software development platform, the latter with software adoption exceeding 50% and quarterly revenue of a few million dollars.

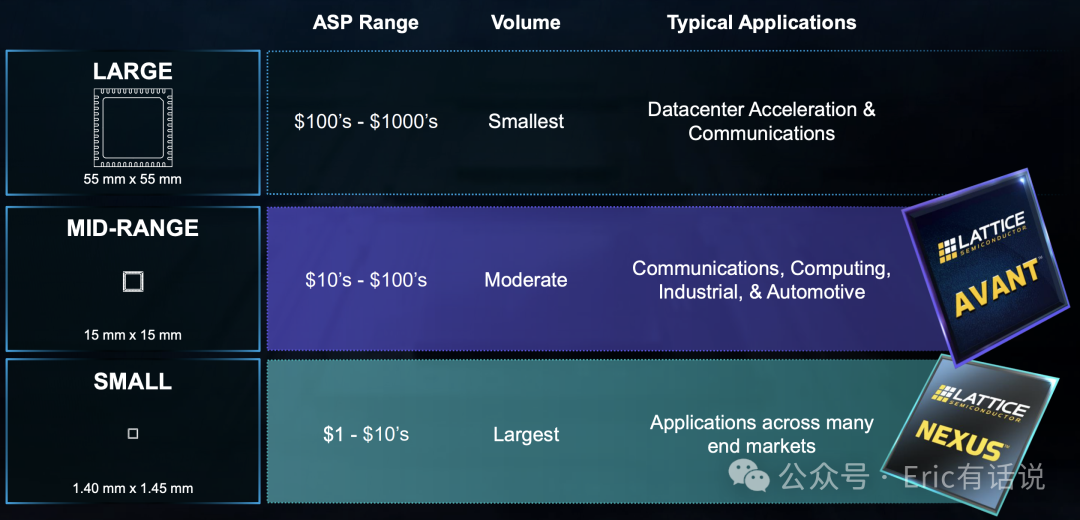

On the FPGA side, the Nexus portfolio targeting the small FPGA market comprises seven series, five currently in volume production with two slated for Q2/Q3 2024 production; Nexus remained the primary shipment driver in 2023, with record design wins.

Last year's new Avant family opened the mid-range FPGA market, with three series (E/G/X), of which the G/X series were just launched in December 2023; Avant E series has begun contributing revenue, with early customer applications focused on communications gateways, industrial control, and LiDAR; Avant E series is expected to ramp in the second half, with G/X series contributing revenue by year-end; 90% of Avant target customers were previously Nexus customers; the software development platform is common across both; Avant products double the company's TAM, with Avant ASP 10-20x higher than Nexus.

AI Exposure:

Current product AI use cases: server control/security chips, PC detection chips, ADAS chips.

In 2023, wireless telecom AI-related revenue was approximately $100M, expected to double going forward.

Outlook:

Q1 revenue guided at $130-150M, down 19%-30% year over year; Non-GAAP gross margin around 69%; Non-GAAP net income around $30-50M; Q2 revenue expected to be flat with Q1; second half revenue better than first half; customer inventory normalization in the second half.

Maintains 2022-2026 revenue CAGR target of 15%-20%.

Valuation-wise, Lattice's sustained high growth in prior years kept its valuation elevated, making entry difficult. The current downturn may present an opportunity. Assuming a trough in the first half and recovery in the second half, full-year Non-GAAP net income of $230M is achievable; at the lower-to-mid range of the 5-year historical valuation (35-60x PE), this implies $8-14B. Per the investor day targets of 15%-20% revenue CAGR, 2025 revenue would be approximately $1.1B with net income around $400M, implying 25x PE.

Of course, projections must ultimately be validated by results. Avant opens Lattice's second growth curve, and its ramp this year could drive upside; the 50%+ per-server content increase is also worth monitoring.