Memory giant Micron kicks off the semiconductor Q1 earnings season. Micron's fiscal quarter is FY26Q2, corresponding to calendar December 2025 through January/February 2026.

Micron FY26Q2 Earnings:

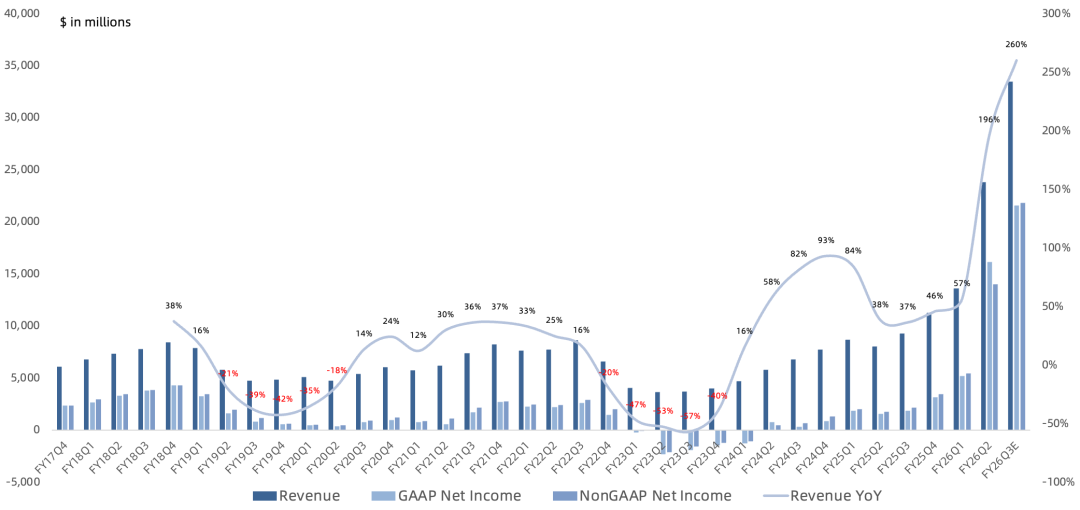

Revenue $23.86B, up 196% year over year, up 75% sequentially, far exceeding consensus of $19.14B; FY26Q3 revenue guided at $35.5B, up 260% year over year, up 40% sequentially;

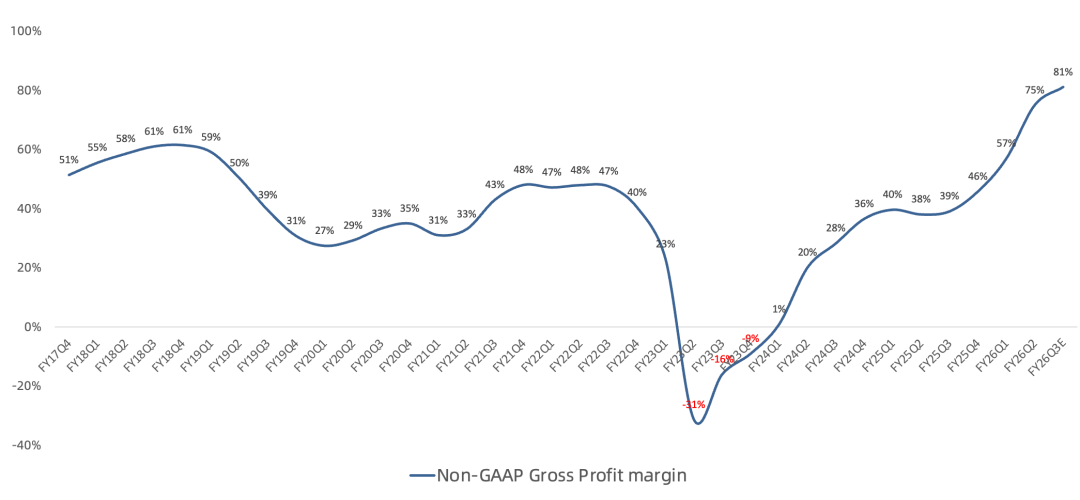

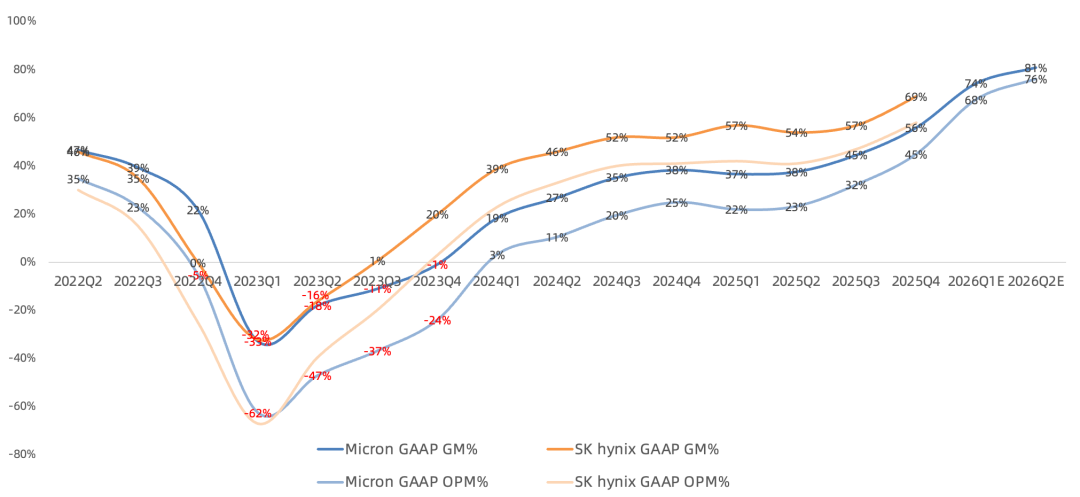

GAAP gross margin 74.4%, up 37.6 percentage points year over year, up 18.4 percentage points sequentially; FY26Q3 gross margin guided at 81%, up 6.6 percentage points sequentially;

GAAP net income was $16.16B, up 921% year over year and 208% sequentially, far above the consensus estimate of $9.82B; non-GAAP net income was $14.02B, up 686% year over year and 156% sequentially, far above the consensus estimate of $9.79B. FY26Q3 GAAP net income is guided to $21.6B, up 1,045% year over year and 34% sequentially; non-GAAP net income is guided to $21.9B, up 903% year over year and 56% sequentially.

The company repurchased $350M in shares this quarter and plans to raise the quarterly dividend by 30%.

Business Segments:

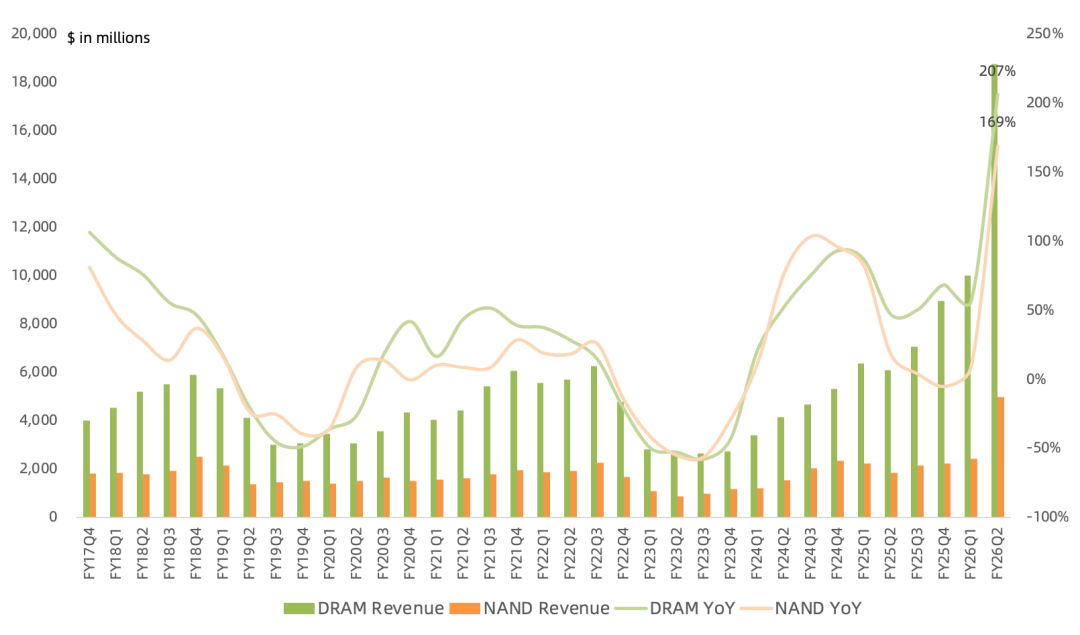

DRAM revenue was $18.77B, up 207% year over year for the 10th consecutive quarter of growth, and up 87% sequentially, representing 79% of revenue. DRAM bit shipments grew mid-single digits sequentially; ASP rose mid-60% sequentially.

NAND revenue was $5.0B, up 169% year over year for the second consecutive quarter of growth, and up 104% sequentially, representing 21% of revenue. NAND bit shipments grew low-single digits sequentially; ASP rose high-70% sequentially.

Clearly, neither DRAM nor NAND growth is driven by shipment volume; it is primarily driven by price increases.

By End Market:

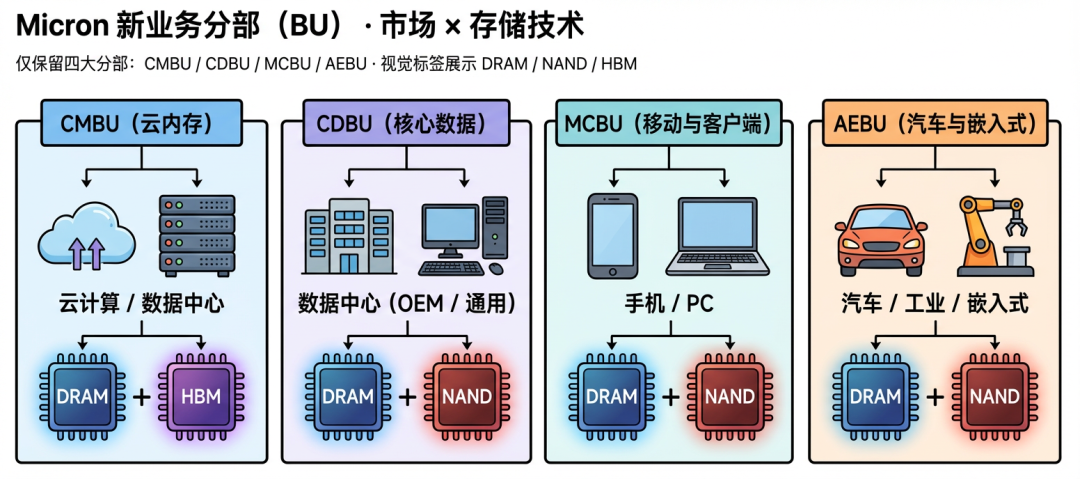

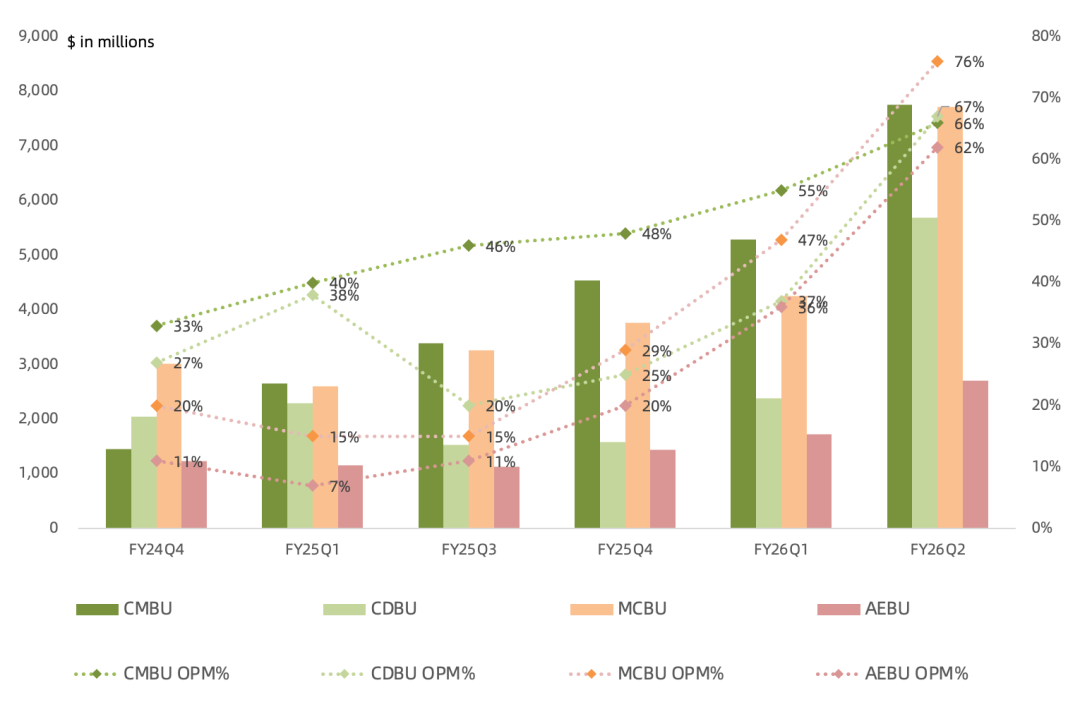

CMBU revenue, represented by cloud customer DRAM and overall data center HBM, was $7.75B, up 163% year over year and 47% sequentially, with an operating margin of 66%, up 11 percentage points sequentially.

CDBU revenue, represented by OEM data center DRAM and overall data center NAND, was $5.69B, up 211% year over year and 139% sequentially, with an operating margin of 67%, up 30 percentage points sequentially.

MCBU revenue, represented by mobile/PC DRAM and NAND, was $7.71B, up 245% year over year and 81% sequentially, with an operating margin of 76%, up 29 percentage points sequentially, surpassing the data center business operating margin for the first time.

AEBU revenue, represented by automotive/industrial/consumer DRAM and NAND, was $2.71B, up 162% year over year and 57% sequentially, with an operating margin of 62%, up 26 percentage points sequentially.

Notably, non-data-center exposure (mobile, PC, industrial, automotive) accounted for 44% of revenue and 46% of operating profit. This segment is purely driven by price increases, not demand, and is the business most vulnerable to the cycle turning point.

Traditional server demand is strong, driven by refresh cycles and Agentic AI demand; AI servers remain robust, with related DRAM/NAND still in short supply. 2026 server shipments are expected to grow low-teens% year over year (slower than 2025), with both AI and traditional servers growing. Server DRAM capacity continues to rise. The industry's first 256GB LP SOCAMM2 based on 1-gamma process has begun sampling. NVIDIA Groq 3 LPX cabinets support up to 12TB of DDR5. Data center NAND revenue doubled sequentially this quarter; NAND demand is expected to remain undersupplied for the foreseeable future.

Management stated that 2026 HBM revenue will be composed of both HBM3E and HBM4 (unchanged). HBM4 36GB 12H entered volume production this quarter, designed for Vera Rubin, with yield ramp expected to be faster than the prior HBM3E generation. HBM4 48GB 16H has begun sampling. HBM4E is expected to enter volume production in 2027 using 1-gamma DRAM process; customized HBM4E products offer differentiated industry options through joint development with customers. Non-HBM margins currently exceed HBM margins.

2026 PC and smartphone shipments are expected to decline low-double-digits year over year. Nearly 80% of flagship smartphones this quarter shipped with 12GB+ DRAM. PC LPCAMM2 completed validation at a major OEM.

Combined automotive and industrial revenue exceeded $2B this quarter. A typical vehicle with sub-L2 ADAS contains roughly 16GB of DRAM, while an L4 autonomous vehicle requires over 300GB.

Earnings Call Highlights:

2026 Micron DRAM bit shipments are expected to grow low-20% year over year (raised); NAND bit shipments are expected to grow 20% year over year (unchanged).

DRAM and NAND undersupply is expected to persist beyond 2026 (unchanged). 2026 NAND capacity growth will be driven primarily by the G9 QLC node, with a new NAND fab in Singapore targeting volume production in H2 2028. DRAM capacity growth will come from expansion: Powerchip's fab transfer completed early, cleanroom expansion at the end of FY26, with volume shipments expected in FY28 (2027). Idaho ID1 targets DRAM volume production mid-2027; ID2 has broken ground. New York fab has broken ground early. Japan fab cleanroom expansion is on track. India assembly and test facility has begun volume production. Singapore HBM advanced packaging fab is expected to release significant HBM capacity in 2027.2027 will see a wave of DRAM/HBM capacity releases.

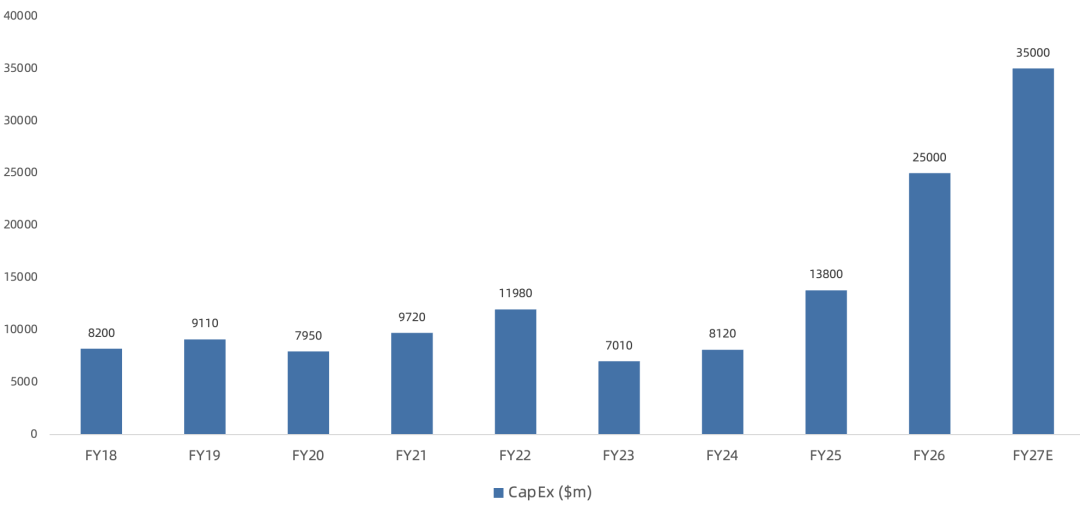

FY26 capex guidance raised to $25B (from $20B last quarter), with the increment primarily for cleanrooms. FY27 capex expected to exceed $35B, mostly related to HBM and other DRAM; equipment spending will also rise significantly. Due to cleanroom capacity needs, construction spending growth is expected to exceed equipment spending growth in FY26 and FY27. EUV usage will increase at the DRAM 1-delta node.

Signed the first 5-year strategic cooperation agreement (SCA). In the mid-term, Micron can only meet 50% to two-thirds of customer demand. Recalling the last cycle peak, management touted LTA share of 70%+ to smooth the cycle, but...

DIO was 123 days this quarter, down only 3 days sequentially, with DRAM DIO below 120 days. Higher prices, lower costs, and a favorable product mix will all contribute to gross margin expansion next quarter. No gross margin guidance will be provided for FQ4.

Overall, Micron's report again significantly beat expectations. Last quarter's report noted that "2026 will truly usher in the explosive earnings period for US AI semiconductors; this year is just the appetizer." We are now witnessing the power of an unprecedented memory supercycle.

Previously noted that with Micron's valuation logic shifting from cyclical to growth, the market needed more positive signals on HBM TAM upgrades. Management finally guided for the $100B HBM TAM threshold to be breached two years early. Long term, Micron's core growth pillars remain HBM, high-density D5/LP5, and data center SSDs. In the near term, however, non-HBM margins have significantly outperformed HBM margins on the back of the price surge.

Management's above-expectation capex and accelerated capacity additions have sparked market concerns about the cycle turning point. The market, and memory makers themselves, know cycles eventually turn. Debating P/E multiples is meaningless. The concentrated DRAM/NAND capacity release node is primarily H2 2027, but the fear is the market starts front-running the turn.