Memory giant Micron kicks off the semiconductor Q1 earnings season. Micron's fiscal quarter is FY24Q2, corresponding to calendar December 2023, January and February 2024.

Micron FY24Q2 Earnings:

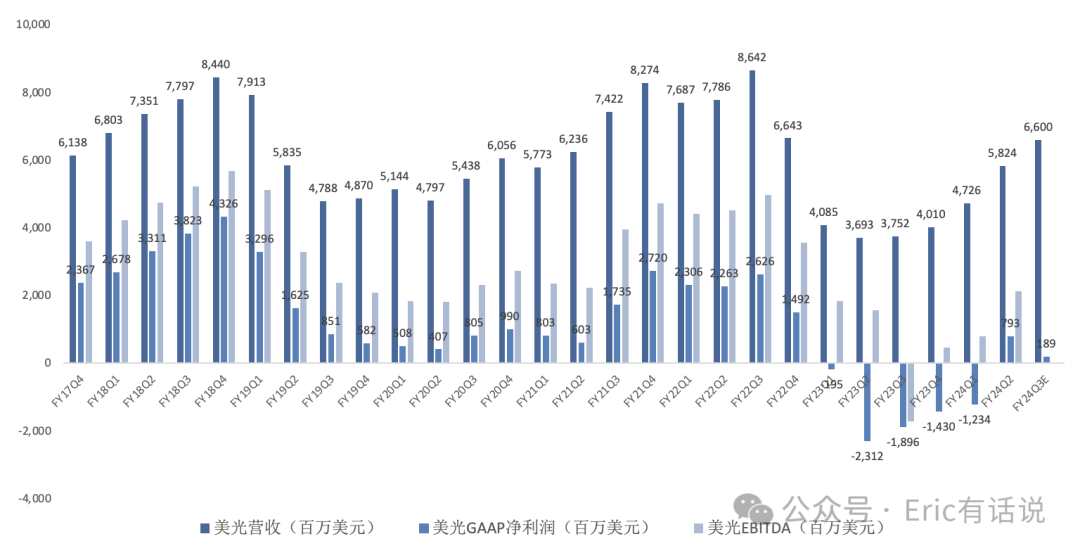

Revenue $5.824B, up 58% year over year, up 23% sequentially; revenue up year over year for the second consecutive quarter; FY24Q3 revenue guided at $6.6B, up 76% year over year, up 13% sequentially (revenue peak was FY18Q4 at $8.4B).

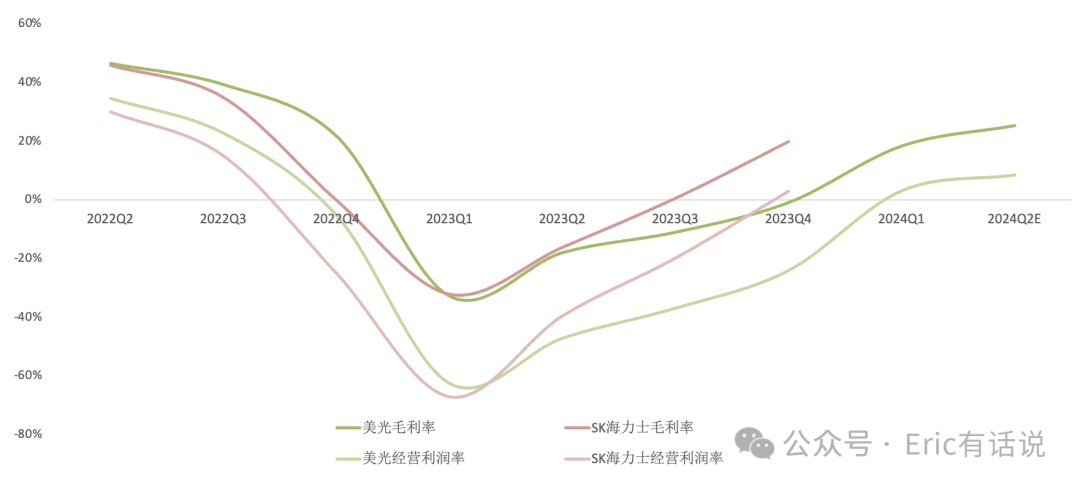

GAAP gross margin 18.5%, turning positive as expected (gross margin peak was FY18Q4 at 61%).

Operating cash flow $1.219B, down 13% sequentially; operating margin 21% (operating cash flow peak was FY18Q4 at $5.2B); free cash flow negative for the sixth consecutive quarter.

GAAP net income $793M, turning positive ahead of schedule; prior quarter loss $1.234B. Non-GAAP net income $476M, turning positive ahead of schedule; prior quarter loss $1.048B. FY24Q3 GAAP net income guided at $189M, Non-GAAP at $500M (net income peak was FY18Q4 at $4.3B).

Business Segments:

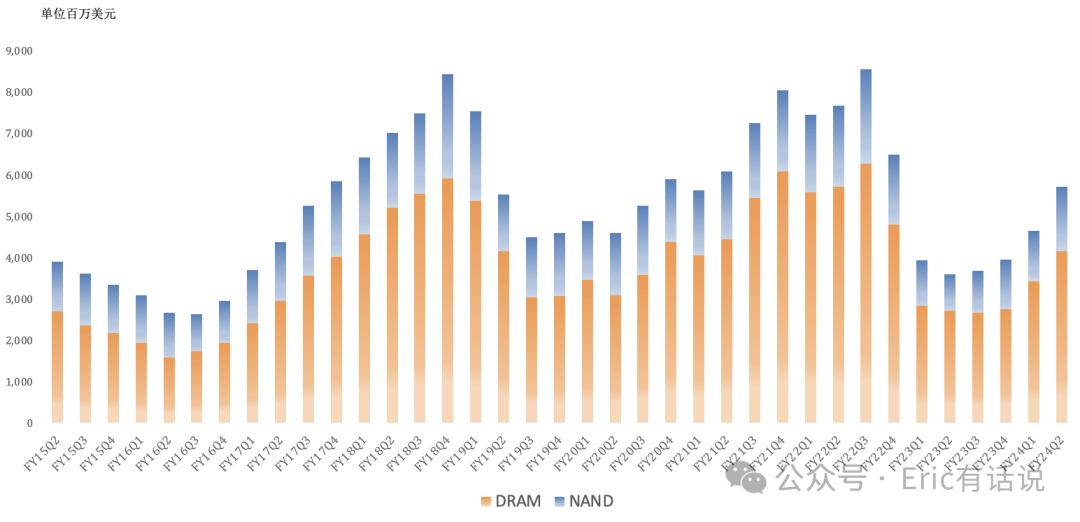

DRAM revenue $4.158B, up 53% year over year, up for the second consecutive quarter, 71% of revenue; DRAM bit shipments up low-single-digits sequentially, DRAM ASP up high-teens% sequentially.

NAND revenue $1.567B, up 77% year over year, up for the second consecutive quarter, 27% of revenue; NAND bit shipments down low-single-digits sequentially, ASP up 30%+ sequentially.

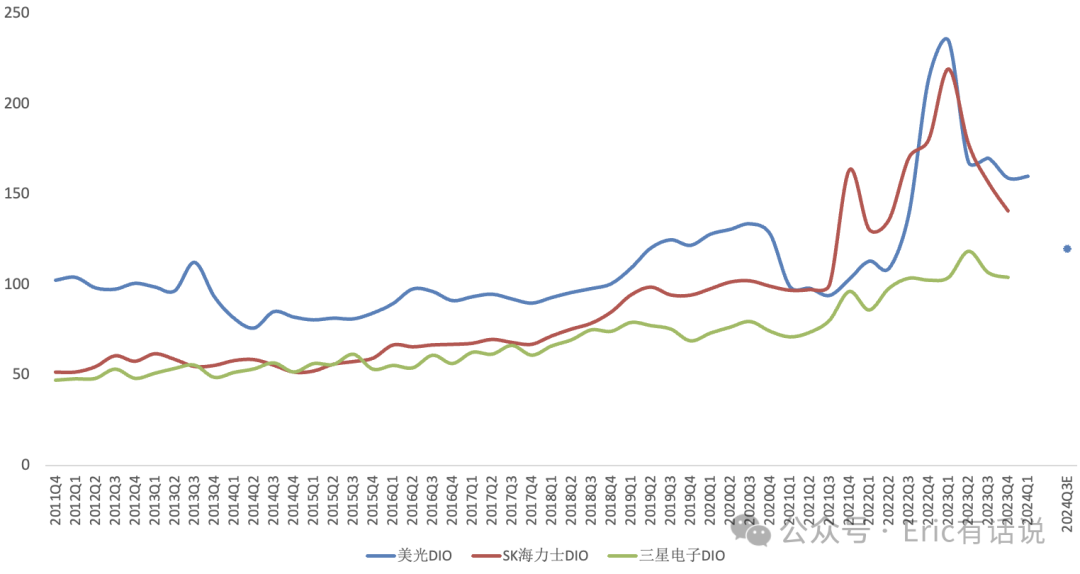

Data center inventory improved significantly thanks to large-scale AI server shipments, expected to normalize in 2024 H1; PC and smartphone returning to growth, auto and industrial inventory approaching normalization.

2024 pricing expected to continue rising; next quarter DRAM bit shipments down slightly sequentially, NAND bit shipments up slightly, but ASP rising, H2 profit to improve significantly; 2025 revenue to hit a new record high.

By End Market:

This quarter CNBU data center revenue grew steadily, cloud revenue doubled sequentially; 2024 server shipments expected up mid-high single digits% year over year (raised), AI servers up significantly, traditional servers up slightly.

HBM3E began contributing revenue this quarter, product consumes 30% less power than peers, shipping to H200; FY24 HBM expected to contribute hundreds of millions in revenue, next quarter to meaningfully help gross margin, 2024 HBM3E capacity sold out, most 2025 capacity allocated; 2025 HBM bit share expected to match company DRAM bit share; 12-high HBM3E sampled this month, DRAM density up 50% to 36GB, expected 2025 ramp.

High-density 1-beta 128GB server D5 module validated, preparing for volume shipments, expected to contribute hundreds of millions in FY24H2; 256GB MCRDIMM module sampling; this quarter SBU data center SSD revenue doubled year over year, 232-layer 30TB SSD revenue up 50%+ sequentially.

2024 PC shipments expected up low-single-digits% year over year (lowered); client SSD QLC bit shipments hit record high, QLC now 2/3 of SSD; AI PC DRAM specs 40%-80% higher than traditional PC.

This quarter MBU shipments declined but ASP rose; 2024 smartphone shipments expected up low-mid single digits% year over year (previous quarter: modestly); AI smartphone DRAM specs 50%-100% higher than non-AI; second-gen 1-beta LPDRAM LP5x + 232-layer USF4.0 NAND sampling.

Auto demand relatively stable, industrial recovering, advanced-node product demand strong.

Earnings Call Highlights:

2024 DRAM bit demand growth expected mid-teens%, NAND mid-teens%; DRAM and NAND supply to remain below demand, DIO continuing to decline; FY24 company DRAM/NAND wafer capacity down double digits vs FY22 peak.

Free cash flow expected to turn positive next quarter.

HBM3E will crowd out traditional DRAM capacity; HBM3E consumes 3x wafers vs same-spec D5, HBM4 will consume even more.

Currently 3/4 of DRAM shipment bits are 1-alpha/1-beta nodes, 90% of NAND shipment bits are 176/232-layer; 1-gamma EUV DRAM and next-gen NAND 2025 volume production on track.

FY24 capex guided at $7.5B-$8B (unchanged), WFE capex continues to decline year over year; Japan, India, China projects advancing, US project pending CHIPS Act subsidies; FY25 capex and WFE capex expected to grow.

Gross margin to turn positive a quarter earlier next year, and price increases will drive full-year gross margin higher; once gross margin returns above 25%, net income has a chance to turn positive.

Overall, Micron beat expectations. While gross margin turned positive on schedule, net income turned positive a quarter early at the 19% gross margin level. Going forward, HBM3E in AI servers and high-density LPD5 will be Micron's two key growth drivers.

Still need to be vigilant: 2024 ex-AI semiconductor may only see a weak recovery; large AI exposure remains the winning formula.